AI and ASX Tech: Moats Didn't Matter

SaaSpocalypse indiscriminately repriced tech companies regardless of moats

This next instalment in my series on AI and ASX tech brings together SaaSpocalypse repricing and moats for durability in the age of AI.

In comparing the moats and share price, the market mostly didn’t discriminate. Companies with multiple strong moats were downgraded alongside companies with limited moats.

The share price of most tech companies took a massive hit in February 2026 (the start of the SaaSpocalypse). But, as the first article in this series observed, the sell-off was mostly down to sentiment rather than recent performance.

The second article in this series looked at the durability of ASX tech companies through the lens of the 8 AI Moats Framework. Each company was scored for how strong its moats were against the moats of data, workflow, regulatory, distribution, ecosystem, network, physical, and scale.

This article brings the two data sets together to provide another lens to try to make sense of this massive revaluation of technology companies.

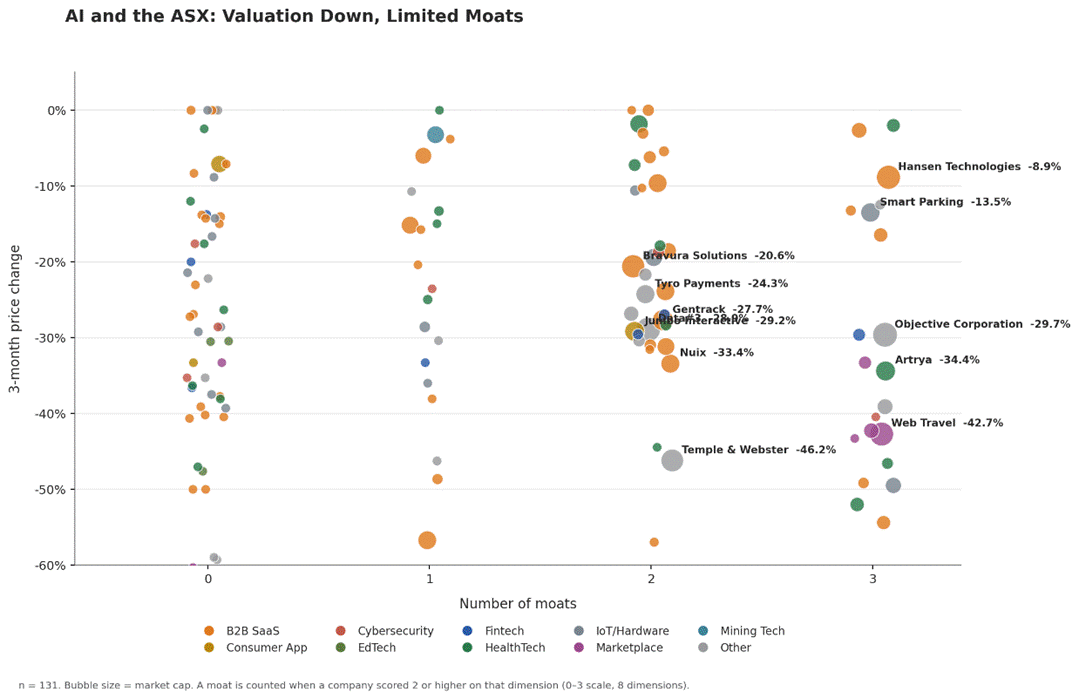

Plotting Moats and Share Price Change

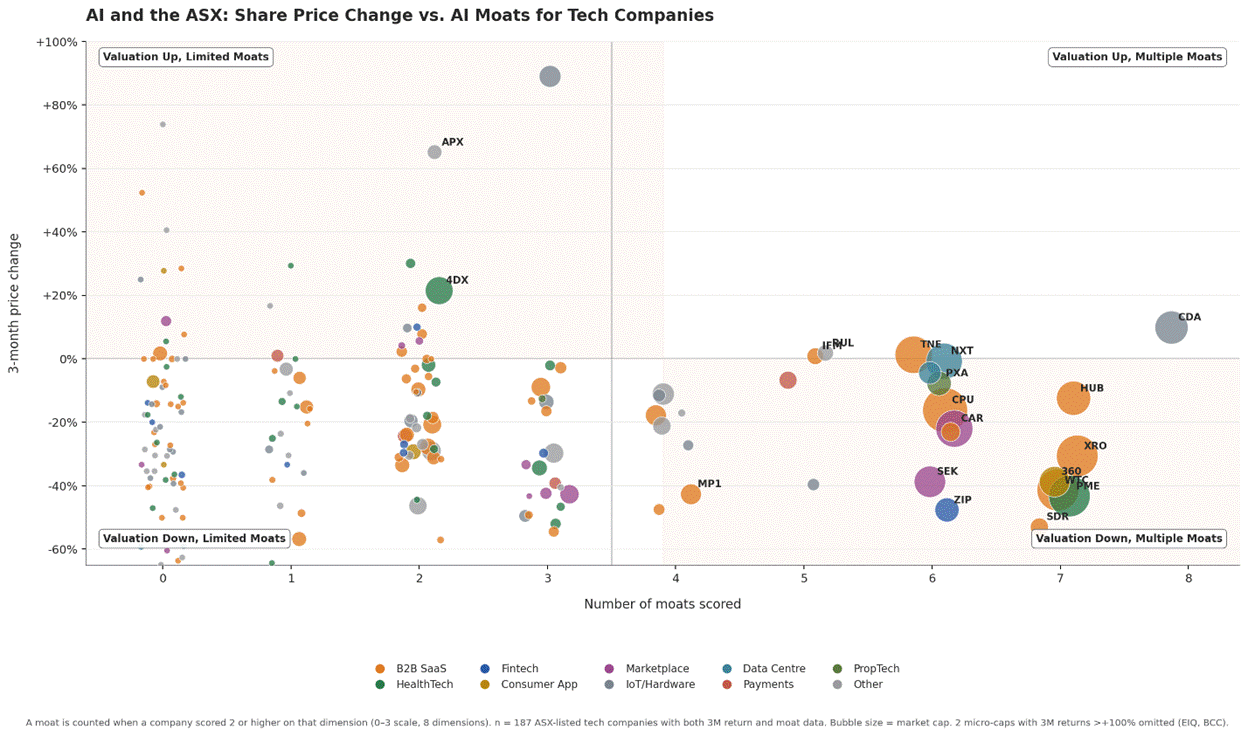

The chart below plots every ASX-listed tech company on two axes:

Figure 1: 187 ASX-listed tech companies. X-axis = number of moats scored 2+ (from the Article 2 scorecard). Y-axis = three-month price change through the February 2026 selloff. Bubble size proportional to market cap.

The chart also divides the companies into four quadrants:

Top-left: Valuation Up, Limited Moats

Top-right: Valuation Up, Multiple Moats

Bottom-right: Valuation Down, Multiple Moats

Bottom-left: Valuation Down, Limited Moats

Let’s zoom in on each.

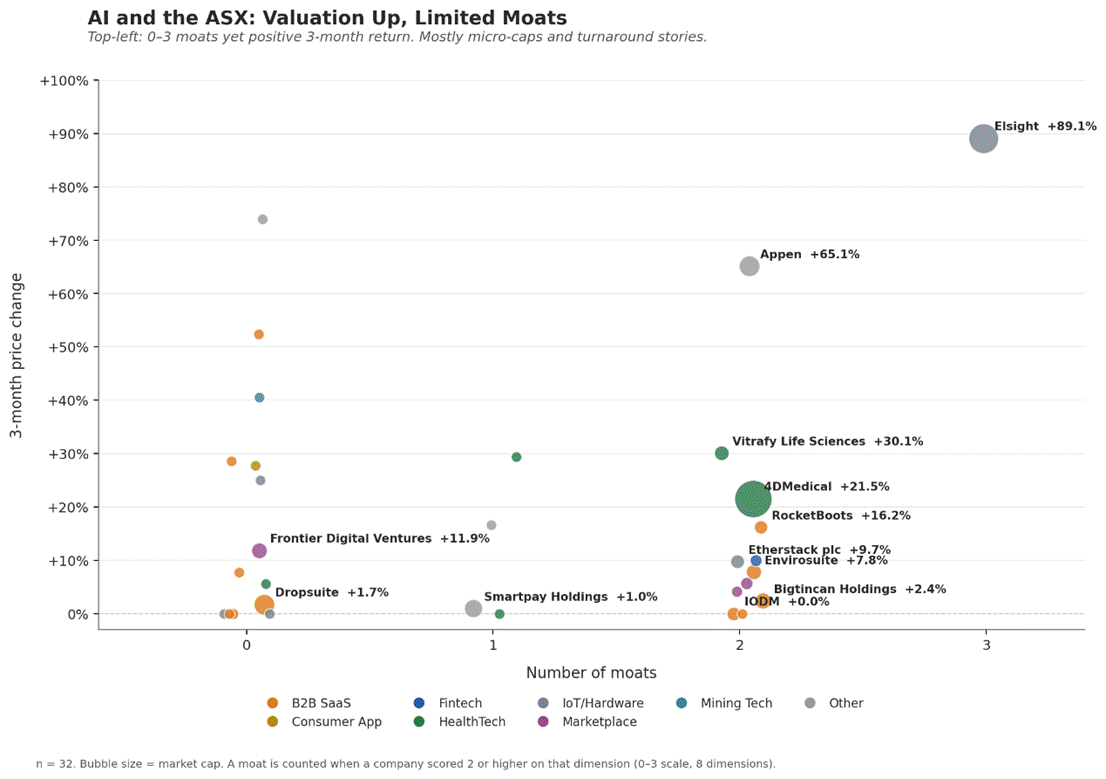

Top-left: Valuation Up, Limited Moats

In the top-left quadrant are companies where the valuation bucked the trend and increased over the SaaSpocalypse even though these companies have limited moats.

A few are probably genuine exceptions that the AI Moats Framework underrates. You don’t necessarily need multiple moats to have a strong, durable company in the future. Having one moat that you’re strong in can carry you a long way and allow you to build more.

The cohort is also heavy on micro-caps which can be more driven by company-specific news rather than a broad AI thesis.

Special Mention: There are two companies that shot up in price so much they had to be clipped from the chart: EIQ at +228%, BCC at +129%.

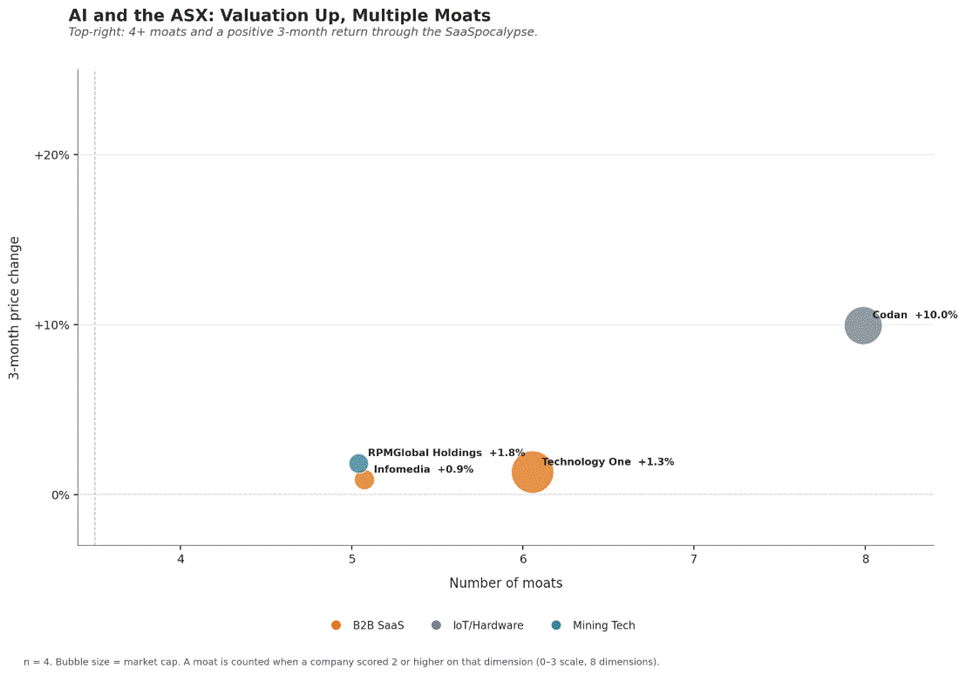

Top-right: Valuation Up, Multiple Moats

The top-right quadrant is the smallest. Only four companies sit in the window: Technology One, Codan, Infomedia, and RPMGlobal. NEXTDC (-0.7%, 6 moats at 2+) sits just below the line.

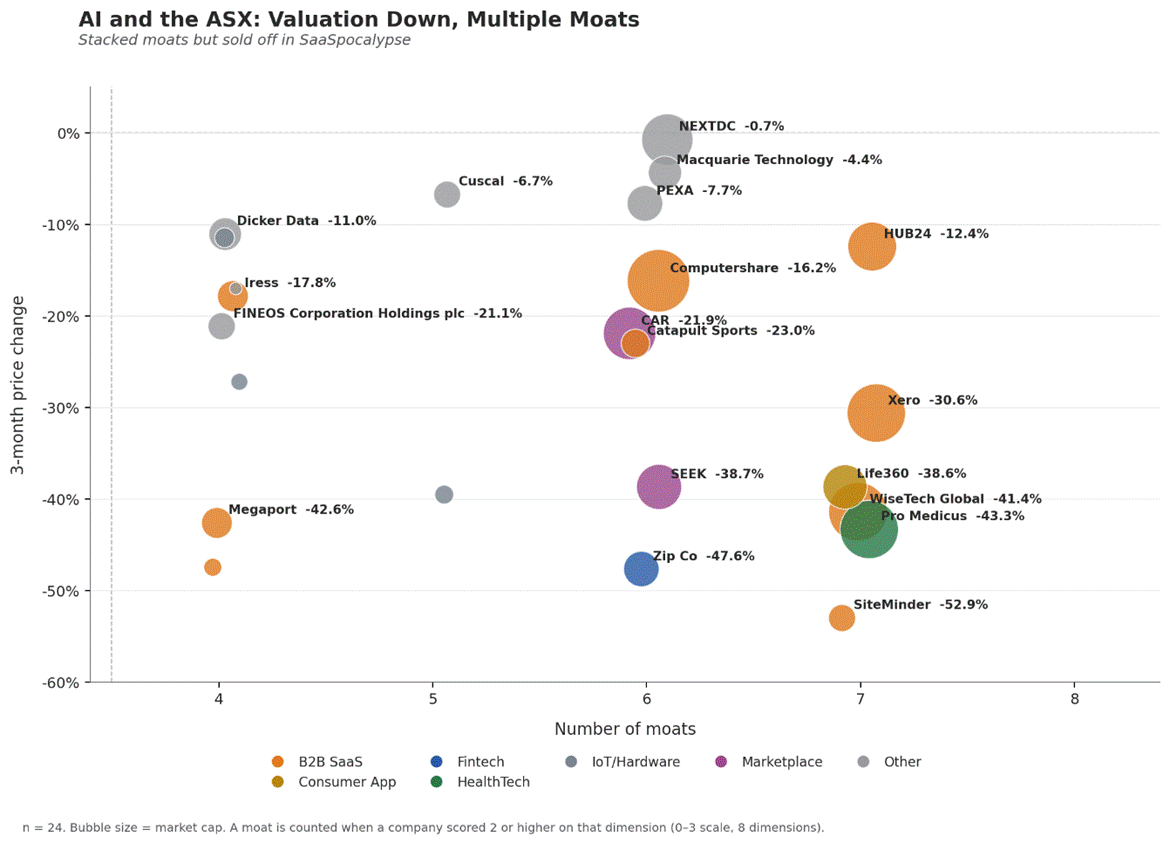

Bottom-right: Valuation Down, Multiple Moats

The bottom-right quadrant is the interesting one. 24 companies that were sold off despite carrying multiple strong moats. These companies are the large, household names of the ASX with a total market cap that is greater than every other quadrant combined.

Seeing all of these with multiple moats sold off, alongside companies with less, reinforces the view that SaaSpocalypse is a broad repricing of technology companies.

Some will turn out to have been mispriced. Over time we will learn which deserved to be repriced and which genuinely faced a threat to durability and future success. This does hint at opportunity being found in a more nuanced analysis per company.

Bottom-left: Valuation Down, Limited Moats

The bottom-left quadrant is the most intuitive and probably least surprising. 125 of the 187 companies had limited moats and were sold off.

This is most of the long tail of micro-cap ASX tech. These are generally smaller companies that are building their way to long-run durability and size.

Key Insights and Questions

Durability against AI didn’t matter in the SaaSpocalypse. Almost everything was repriced. This lines up with our findings in an earlier article that showed the disconnect between recent performance and share price movement.

Outside of that, this analysis raised more questions than it answered:

Are all moats created equal? Perhaps the number of moats is not the greatest predictor of future performance. Maybe some moats are going to be stronger than others up against AI. While I’m hesitant to draw too many conclusions, beyond SaaSpocalypse being a mass repricing, this does bring me to my next question:

What is it about the companies with limited moats but increased share prices? The companies with a limited number of moats and increased share prices over the SaaSpocalypse may have some interesting insights for us around market views on AI. Do they share a set of moats? What’s driving the price? With their smaller size it will likely be easier to pinpoint what is driving price changes and therefore how the market is thinking about AI. A topic for a later post in the series.

Is out-performance against AI to be found in smaller companies for tech investors? The chart would seem to suggest it’s an interesting line of inquiry.

Next in the Series

As you can tell, we still have more questions about the SaaSpocalypse to explore.

Now that we’ve broadly covered valuations and moats, the next few articles will look at more specific insights and relationships in the data.

Notes:

Drawing the line: I’ve used “four or more moats at 2+” as the moat-stacking threshold and “zero” as the price threshold. Different cutoffs would shuffle a few names — NEXTDC and 4DMedical are the most obvious — but the four-quadrant pattern is robust to the choice. The point is the relationship between the views, not the borders between the quadrants.

Number of companies: Keen regular readers will note that in the last posts we had 201 companies. Only 187 were used here because 187 of the 201 scored companies have both three-month return data and moat scores. Excluded names were missing one of these, usually the return data due to being thinly traded or for other reasons.