Deep Dive: Carma at $0.90. Cheap or Priced Correctly?

Full stack used car sales platform shows promise but needs more scale and cash

Carma is a “full-stack” used-car sales platform that has grown relatively quickly and recently listed on the ASX. The full-stack model, designed to replicate the success of Carvana in the United States, handles buying then selling cars through a few clicks, refurbishment services and seamless physical outlets.

Carma’s managed to build up a sizeable revenue base and seems set to grow it further this financial year. It’s burning cash and will need to keep going for a few more years to get to the scale it needs.

It’s clearly found product/market fit in Australia and an operational cadence. Carma’s also shown strong operational execution to do this over a relatively short time frame.

If Carma can replicate just some of the success of Carvana then there is a substantial business and plenty of upside. But, anything other than fairly rapid growth from here could be challenging.

About Carma

Company was founded in 2021 by Lachlan MacGregor and Yosuke Hall to disrupt used car sales in Australia by “replicating the online, full-stack model that we see achieving success in the U.S. and globally”. In other words, to replicate the success of Carvana’s model, challenging the dominance of incumbent carsales.com.au.

The “full-stack model” is about owning the entire end-to-end journey for buying a used car online. Find the car you want, hit buy, have it delivered or picked up without any of the negotiation hassles, pick-up coordination issues or post-purchase worries.

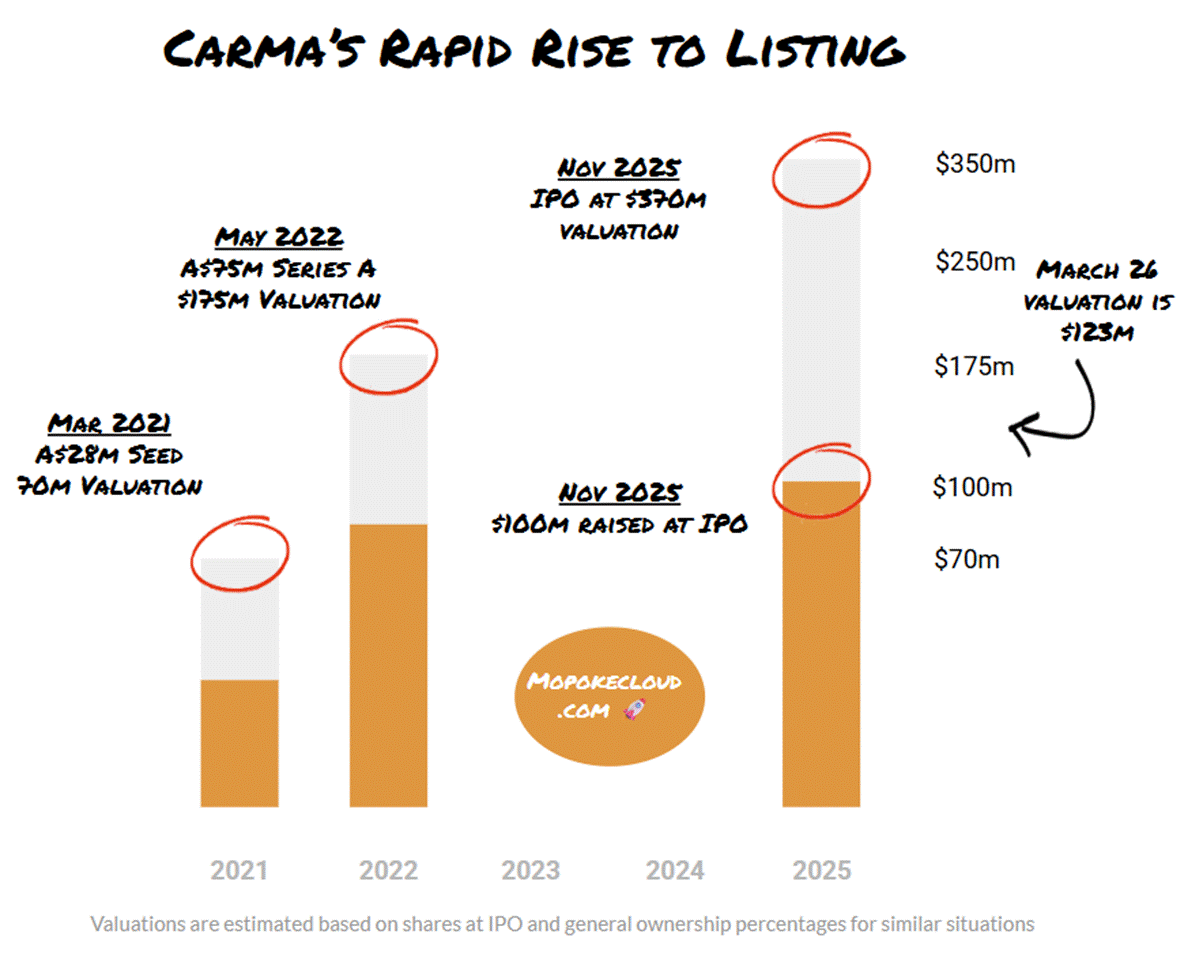

Carma came out of stealth in 2021 with a massive seed round of A$28m from Tiger Global. Since then it has raised A$133m from investors like Regal Funds Management, General Catalyst and Five V.

Interestingly, A$30m of this was a Convertible Note in the 6 months before the IPO, rather than an equity investment.

Carma listed on the ASX in early November 2025 at $2.70 per share, raising $100m with a market capitalisation of $370m. The share price has since fallen to $0.90 (as of 25 March 2026).

A back-of-the-napkin estimate says the last priced round, the Series A, would have been at about a $190m-$375m valuation. So the listing price represented as high as a 48% premium on the Series A valuation but today’s market capitalisation of ~$123m is possibly below the valuation Series A investors invested at.

Business Model

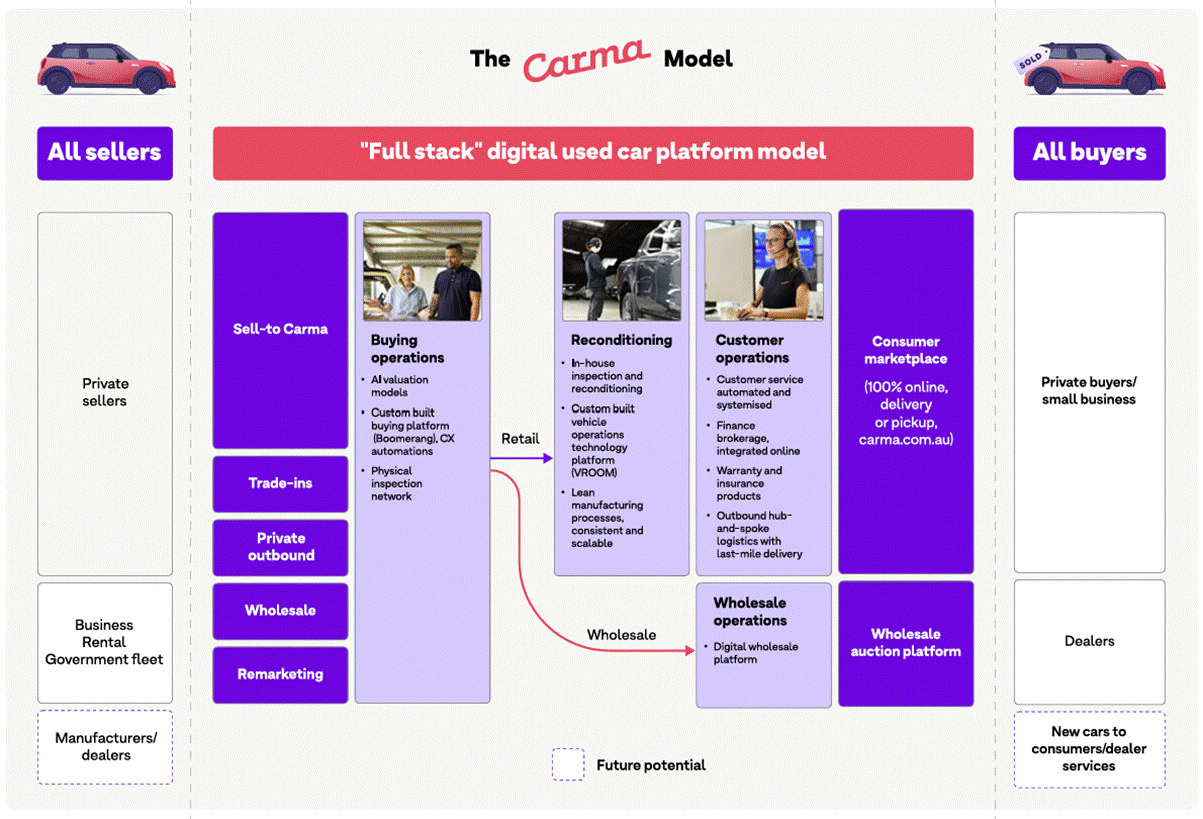

In practice the “the full-stack business model”, driven by an online experience, is about how Carma handles every step of the journey in buying or selling a used car.

The “full-stack” line is also in comparison to the typical digital classifieds model where the website, like carsales.com.au in its most popular form, only takes care of the listing and puts responsibility of everything else on the buyer and seller.

Carma’s prospectus contains a great diagram that illustrates their business model well:

The implications of this model are worth considering, relative to the online classified model. The full-stack model is taking risks on:

Pricing of the car when purchasing: if they pay too much they lose money on the sale, if they pay too little then people won’t want to sell to them. Doing this at scale requires some strong systems and pricing models, particularly if a car needs reconditioning.

Carrying of stock: the beauty of the online classified model is that you have no stock. The full-stack model means holding inventory that you may or may not sell. You also need somewhere to keep it.

Reconditioning the car: fixing or touching up the car to increase the sale price or make it sale worthy isn’t necessarily difficult on its own but requires strong systems at scale. Not only that, it requires a good network of skilled suppliers who can perform the reconditioning work. Balancing outsourced, in-house employment of these skills at scale isn’t an easy task.

Delivery to the customer: the end delivery to a customer requires additional effort and coordination. Though this is a fairly solvable area, relative to the risks and additional costs listed above.

Each of these has been solved by others, particularly Carvana. Solving them opens up the potential of this opportunity. However, they represent important considerations as Carma grows, beyond those of an online marketplace.

Market

Geographically Bound

The market for the car marketplaces has proven to be geographically bound. By looking at the various mature players globally, like carsales, cars.com and autotrader, they have all ended up with geographic boundaries defining their subsidiary marketplaces.

Here is a slide from Car Group on how they address different markets with different businesses:

If you look at Carma’s directly comparable business, Carvana, it has remained focused on the US. While the US is a bigger market, the infrastructure, market intelligence and networks that a Carma style business model needs to be successful point to Carma needing to be Australia focused in the short-to-medium term. This isn’t necessarily a bad thing, Carvana produces significantly more revenue in the US than its peers.

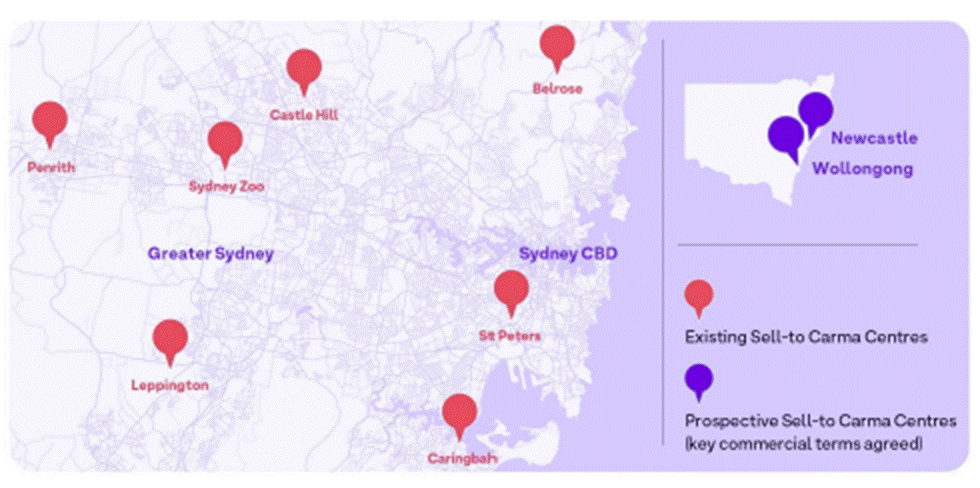

Carma is even a little more geographically bound, it is currently only operating in Sydney. But for our purposes here, we will consider the total market as Australia.

The Australian Market

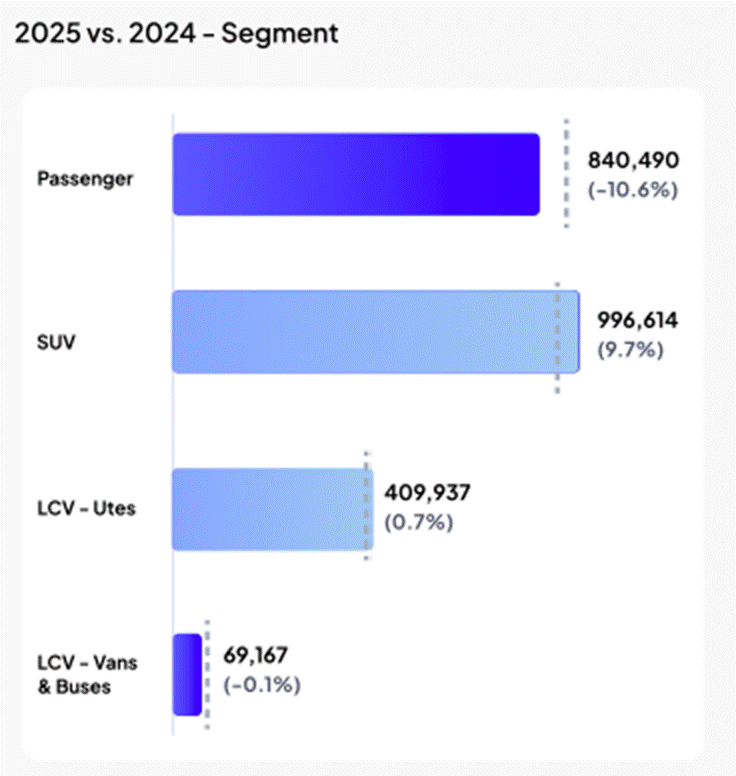

In 2025, 1.21m new cars were sold in Australia (source: Federal Chamber of Automotive Industries) and 2.32m used cars were sold (source: Annual Automotive Industry Report). Passenger cars and SUVs make up the majority of sales, followed by utes.

Used Car Sales in 2025 from the Annual Automotive Industry Report

Sales are highly fragmented. No single dealer group holds more than ~6% and many individuals sell their cars via carsales.com.au.

Competition

Online Classifieds: Carsales.com.au

Carsales is the giant in the room, with a dominant market share of used cars listed and sold. There are others like Gumtree and Drive.com.au but they have a small share relative to Carsales.

Carsales market share is a little difficult to ascertain, but they do publish that they have “78% share of time against competitors”.

Carma uses carsales.com.au and other classifieds to advertise, arguing that Carsales is an advertising channel for them. But, Carsales is also trying to provide a more seamless purchase experience akin to what Carma uses.

Carsales is on a slightly different strategy to Carma. Carsales is focused on “making buying and selling vehicles a great, seamless digital experience”. However, the trouble with a pure digital experience is that it isn’t seamless. Users feel hassled and don’t get the car sold seamlessly. Yes, Carsales does provide for instant trades but they aren’t investing in the full-stack experience. For more on this, read my deep dive analysis of Carsales strategy.

Dealerships

Carma also competes directly with dealerships selling and buying new and used cars. Most sell new and used.

Dealers have advantages in that they are physically present in many locations already, they provide (or purport to provide) a higher level of service, and they may have exclusive arrangements with brands people desire.

Dealers also have disadvantages. Research conducted on consumers by Frost & Sullivan found buying from physical dealerships (both new and used) highlights that pressure to sign immediately (32%), long wait times (30%) and lack of product knowledge (28%) are among the most common complaints at dealerships.

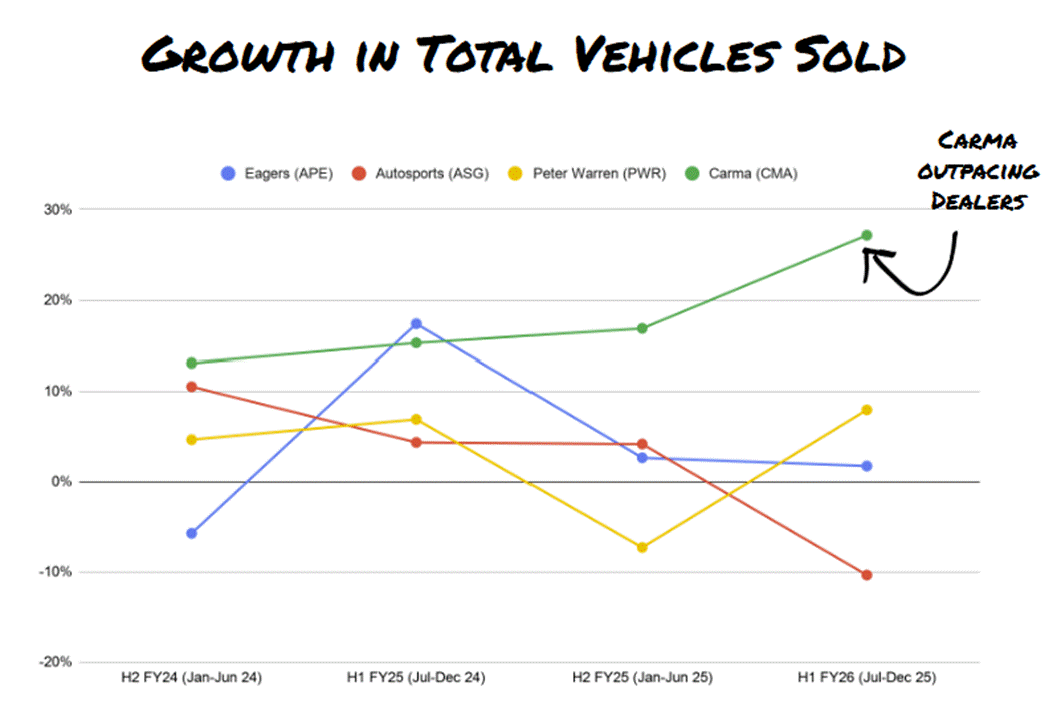

Listed automotive groups Eagers, Autosports and Peter Warren provide some insights into the market because they need to publish information.

Here is a chart of the growth rate of each business by half year for total vehicles sold:

Full Stack, Global Peers

It’s tempting to consider Carma’s global peers like Carvana, AUTO1 and Constellation Automotive as potential competitors as they may want to enter the Australian market. However, given the way the digital car marketplaces have played out it is much more likely that they will look to acquire Carma, particularly given the additional on-the-ground infrastructure the Carma model requires.

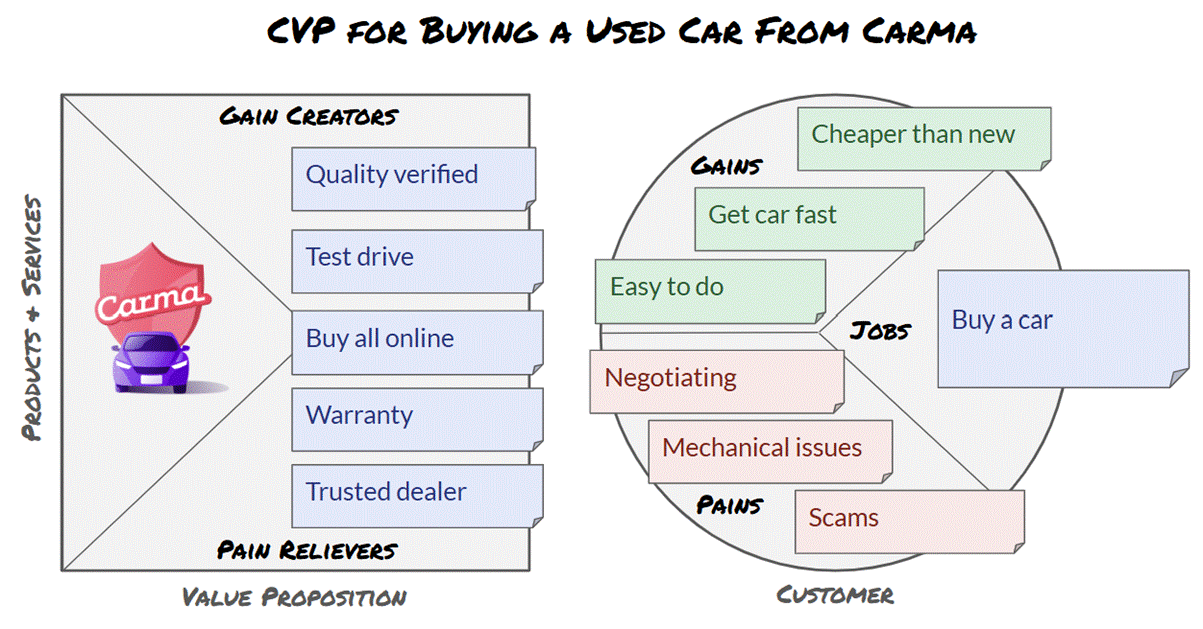

Customer Value Proposition

The real job-to-be-done for customers is to buy or sell a car. When buying second hand, reliability and quality are cited as the most important purchase criteria (according to Frost & Sullivan). Carma attempts to deliver on this in a frictionless online buying experience that transitions into physical reality in a low stress way.

Product

Carma’s core product is the end-to-end used car transaction — both buying from consumers and selling to them — delivered through a seamless digital interface backed by physical operations.

On the sell side, customers receive an instant online offer for their car, with Carma handling pick-up logistics. On the buy side, customers browse an online inventory of inspected and reconditioned vehicles, with home delivery and a return window (akin to Carvana’s 7-day policy) reducing the typical anxiety of buying used. This return policy is a meaningful product differentiator — it shifts the trust burden from the buyer to Carma, which in turn places pressure on the quality of Carma’s reconditioning and inspection process.

The technology platform underpinning these experiences — pricing algorithms, inventory management, reconditioning workflows — is where Carma is investing meaningfully (including the $2.7m of capitalised software development noted in their financials). This platform is a key source of potential competitive advantage as it scales, but remains largely unproven at higher volumes.

Go-to-Market

Carma’s go-to-market is heavily centered around the physical locations of its facilities. These are currently around Sydney with plans to expand to Newcastle and Wollongong next. These facilities are needed to buy, verify, refurbish and sell the cars.

Their primary go-to-market channels are social media, sponsorships, partnerships, outdoor advertising and, interestingly, classifieds platforms (including carsales, drive.com.au and gumtree). There is this little line in the Prospectus section Key Risks for Carma, the business depends heavily on advertising and classifieds platforms to attract and retain customers.”

They also put little “carma” logos on some of the cars they sell.

Over time they will likely expand into less facility heavy modes of delivering their service like Carvana has, but for now this is how Carma is operating.

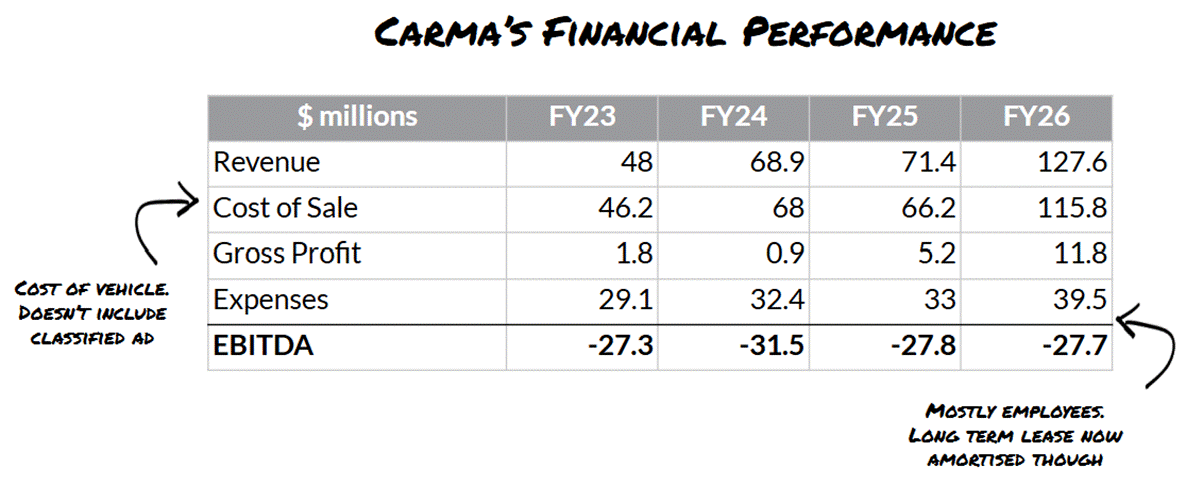

Finances

Carma is making substantial losses, with quite thin gross margins in pursuit of a large volume of sales. Revenue was flat over FY24/FY25 but is expected to jump over FY26 and the half-year results support this.

The key points of interest with their financials are:

Their cost of sale doesn’t appear to include the direct classified costs for a car sold.

Their occupancy expenses drop significantly in FY26 even though the number of locations they are occupying is growing. This is largely due to the lease being amortised as a long-term lease.

They appear to be capitalising a few operational parts of their business:

$2.7m of software development

$2.6m for “reconditioning” and upgrading their St Peters facility.

New facility costs

It will be interesting to understand the costs involved in setting up a new facility as they continue to report financials over time. This is a key ingredient in the costs to scale and grow.

Valuation

At $0.90 per share, Carma trades at a market capitalisation of approximately $123m. Against FY26 revenue of ~$127m, that implies a price-to-sales multiple of roughly 1x. But, the revenue multiple alone isn’t that useful in valuing the business.

Carma needs to grow revenue more than 4x from here to reach its ~$550m breakeven threshold based on current margins. If it can’t get there or takes longer then generating profits is going to prove challenging.

There are three scenarios that help us think about valuation:

1. Bull Case: 47% Growth Continues to Breakeven

2. Base Case: Moderate Growth (15% annually)

3. Bear Case: Flat Revenue, Restructure Required

It’s also useful to compare to Carvana, so we will include that as well.

Bull Case: 47% Growth to Breakeven (~FY30)

This scenario models the Prospectus trajectory: 47% compound revenue growth from the FY26 base of $127m. At that rate, Carma crosses the ~$550m breakeven threshold in FY30, approximately four years away.

This will almost certainly require an additional cash injection beyond Carma’s current cash at bank.

By the end of FY30 (in 4 years) Carma would be at about $593m revenue with a 5% EBITDA margin. Carma would generate ~$30m EBITDA. At a 15x multiple (a reasonable premium for a profitable growth business), that implies an enterprise value of ~$450m which is roughly 3.5x the current market cap. The upside is real, but it is entirely contingent on sustained 47% revenue growth across four years and an additional capital raise at acceptable dilution.

Base Case: Modest Growth (15% Annually)

This scenario looks at how more modest growth might impact the outcomes of the business.

There are a variety of reasons why growth might be more modest. For instance, Carma has had a flat period in very recent history (FY24/FY25) or competition might become more intense.

At a more modest 15% growth, which is somewhat more generous than the flat FY24/FY25, it will take until approximately FY37, which is eleven years from today, to reach breakeven without any cost restructuring.

Even with cost restructuring, the gross margins make it challenging to achieve an EBITDA number meaningful enough to get to a $123m valuation.

Bear Case: Flat Revenue, Restructure Required

In this scenario, revenue stalls at $127m after FY26, like it did over FY24/FY25, and Carma is forced to restructure to survive.

At 7.3% gross margins on $127m, gross profit is approximately $9.3m. It is important to note here that a 10% EBITDA margin on $127m revenue ($12.7m) is mathematically impossible at 7.3% gross margins.

EBITDA can never exceed gross profit regardless of how aggressively costs are cut. The maximum EBITDA achievable in a flat-revenue scenario is bounded by the $9.3m gross profit ceiling.

If management cuts OPEX beyond $3-5m at these numbers, then this would likely mean a reduction in facilities which would hurt revenue.

In a restructured bear case producing ~$4–5m EBITDA from the current revenue, at a 10x EBITDA multiple, the implied enterprise value is ~$40–50m. This is not only difficult to achieve but below the current valuation.

Carvana Comparison

Carvana is the most instructive comparable. After near-bankruptcy in 2022, it restructured its debt and by FY2024 was generating approximately $1bn+ in EBITDA on ~$18bn revenue (an EBITDA margin of roughly 5–6%). Its market capitalisation now sits in the $45–55bn range, implying an EV/EBITDA multiple of approximately 40–50x, reflecting market leadership and a growth premium. On a price-to-sales basis, Carvana trades at roughly 2.5–3x revenue.

Applying Carvana’s 2.5x revenue multiple to Carma’s current $127m revenue would suggest an enterprise value of ~$318m which is 2.5x the current market cap. But this comparison is premature: Carvana earned its multiple by achieving profitability and demonstrating the model at scale. Carma is at least four years and a capital raise away from being in that position, and in a market roughly 140x smaller.

Key Insights

There is clearly demand for a service like Carma, overseas businesses like Carvana have proven it. The revenue growth for Carma is further validation of this product/market fit.

Growth in the company’s valuation relies on the substantial growth story coming true.

Carvana at scale makes for a good comparison and illustrates the potential of where Carma can go, including with add-ons like finance, there is still a ways to go, potentially dilutive funding rounds and competition to beat to get there.