Deep Dive: SiteMinder

ASX SDR keeps growing but the share price is up one minute, down the next. Is this the beginning of a long run up and to the right?

SiteMinder is a great example of a global market leader built in Australia, listed on the ASX.

Its valuation fortunes have risen and fallen with what seems to be a few non-operational issues and external market forces, all while its core operations have continued to grow and grow.

SiteMinder keeps delivering growth year after year, but it might be on the cusp of growth and profits.

This deep dive looks at SiteMinder, one of the many software companies devalued in the SaaSpocalypse (the AI-driven sell-off) of early 2026.

SiteMinder has recently seen a jump in share price and recently announced a new model for distributing its product within a key partner’s platform.

This deep dive covers the usual aspects of the business:

About the Company

Product: A Well-Segmented Platform

Business Model: Simplifying Cost and Complexity of Hotel Bookings

Customer Value Proposition

Market: Room To Grow

Competition: Or Co-Opetition?

Go-to-Market: Standard SaaS Mix

Finances: To Profit or Not To Profit

Key Risks and Scenarios

Valuation

Bonus: if you’d prefer to listen to an entertaining, argumentative but less analytical deep dive then tune into The Contrarians to hear me debate SiteMinder with Adam Schwab and Adir Schiffman to an audience of 40,000+ listeners.

About SiteMinder

SiteMinder was founded two decades ago in 2006 by Mike Ford and Mike Rogers. Mike Ford spotted an opportunity for software to help him better manage his backpacker business’s accommodation across online travel agents. He partnered with Mike Rogers, a software engineer, to pioneer the channel management software category.

Les Szekely, a former Horwath/Deloitte partner, had direct experience with the shift to digital booking and got involved as the first investor and board member. The amounts Szekely invested early aren’t clear, but he remained a board member up until December 2025, so has clearly played a key role in the growth of the company as well.

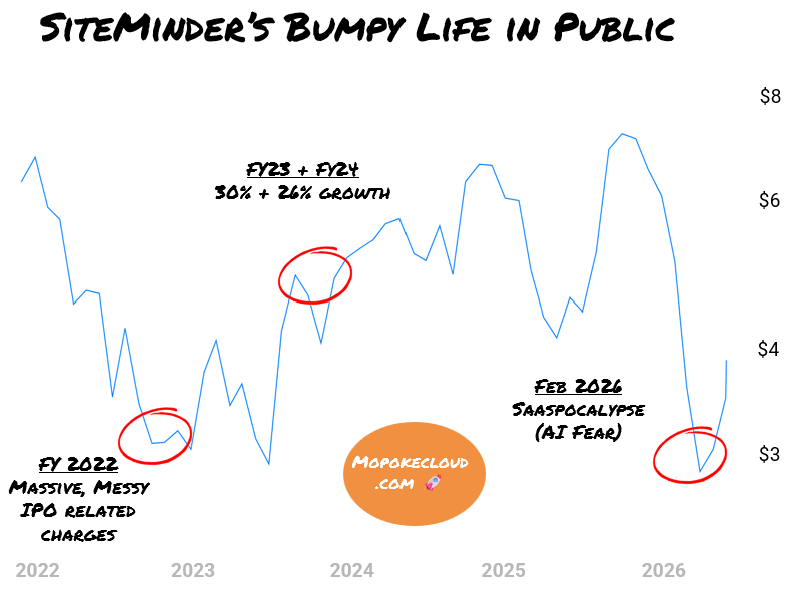

The company went public in 2021 and it’s had a bumpy life in public since:

Mike Ford stepped out of day-to-day involvement in the company with the appointment of Sankar Narayan as CEO in January 2019. Narayan joined from Xero, where he was CFO then COO for around 3 years of impressive growth.

Narayan has been the CEO for over 7 years now, which likely provides an element of stability.

Product: A Well-Segmented Platform

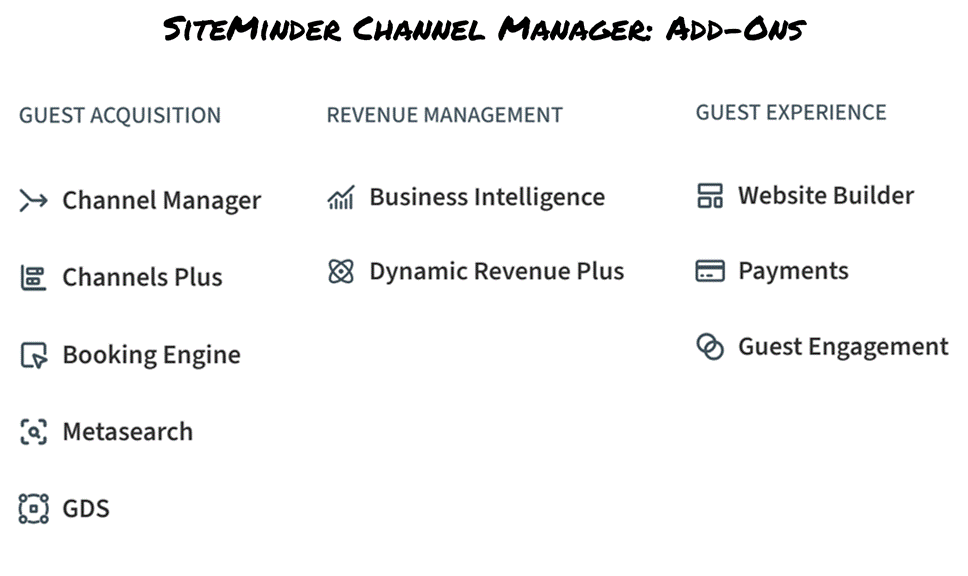

SiteMinder has two core software-as-a-service products Channel Manager and Little Hotelier that are for accommodation providers (e.g. hotels, bed & breakfasts, motels, holiday parks).

Channel Manager

Channel Manager, often referred to in the market just as SiteMinder, helps hotels to acquire guests, improve revenue, provide a better guest experience and improve operations. It is deliberately not for managing the property itself. Instead, it connects to a hotel’s existing hotel/property management system and helps move inventory through the many different channels (e.g. booking.com, trivago).

The core, original product for publishing rooms and synchronising bookings across multiple channels is the essential foundation. Then with this in place customers can use add-ons with different price points and pricing mechanisms to increase their revenue and bookings

Little Hotelier

Little Hotelier is a standalone all-in-one hotel management product called Little Hotelier that is targeted at small (even micro) accommodation. It is a simpler product that gives a property with a small number of rooms the ability to manage everything they need in one place, including managing the property itself.

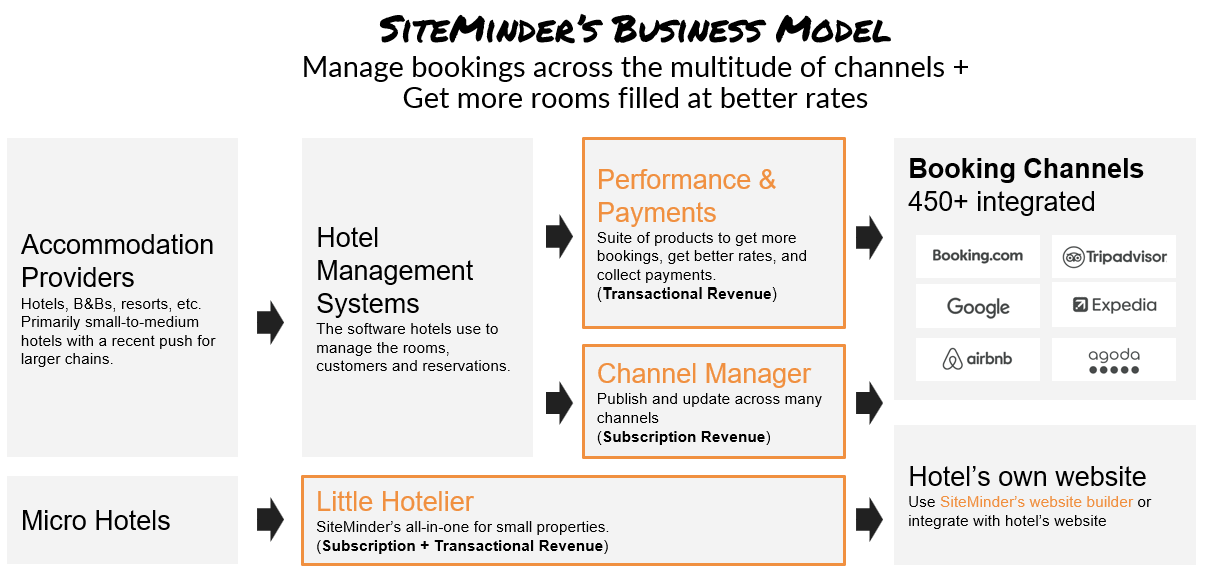

Business Model: Simplifying Cost and Complexity of Hotel Bookings

SiteMinder’s business model centres around the challenge accommodation providers (e.g. hotels, resorts, bed & breakfasts) have in managing their inventory – their available rooms – across the multitude of booking channels that are available. This core problem also leads to the opportunity to improve occupancy rates and optimise revenue.

SiteMinder charges a recurring subscription fee for some of its software products (Subscription Revenue in their reports) and charges a performance fee where SiteMinder more directly helps make a booking (Transactional Revenue).

The base Channel Manager product is a subscription that is priced by the number of rooms that will be under management. Customers can then add payment processing (SiteMinder takes a clip), channel optimisation and other revenue optimisation products where SiteMinder takes a commission. The core product relies on the accommodation having a hotel management system in place, which is something most small-to-medium accommodation providers will already have.

Little Hotelier has a simple recurring subscription fee with some transaction and commission based add-ons like the Channel Manager.

The software subscription has proven to be resilient, holding well during COVID. Whereas the performance-based, transactional products are tied to outcomes (bookings).

The software subscriptions are on higher gross margins of 85%+ while the transactional products have margins of ~30-60%+ (seems to vary per transactional product). As transactional revenue grows (its growing faster than software subscriptions) the total gross margin of the business will decline. However, the combination of the two likely provides greater stickiness with customers as it is hard to switch off a product that you only pay for when it brings revenue.

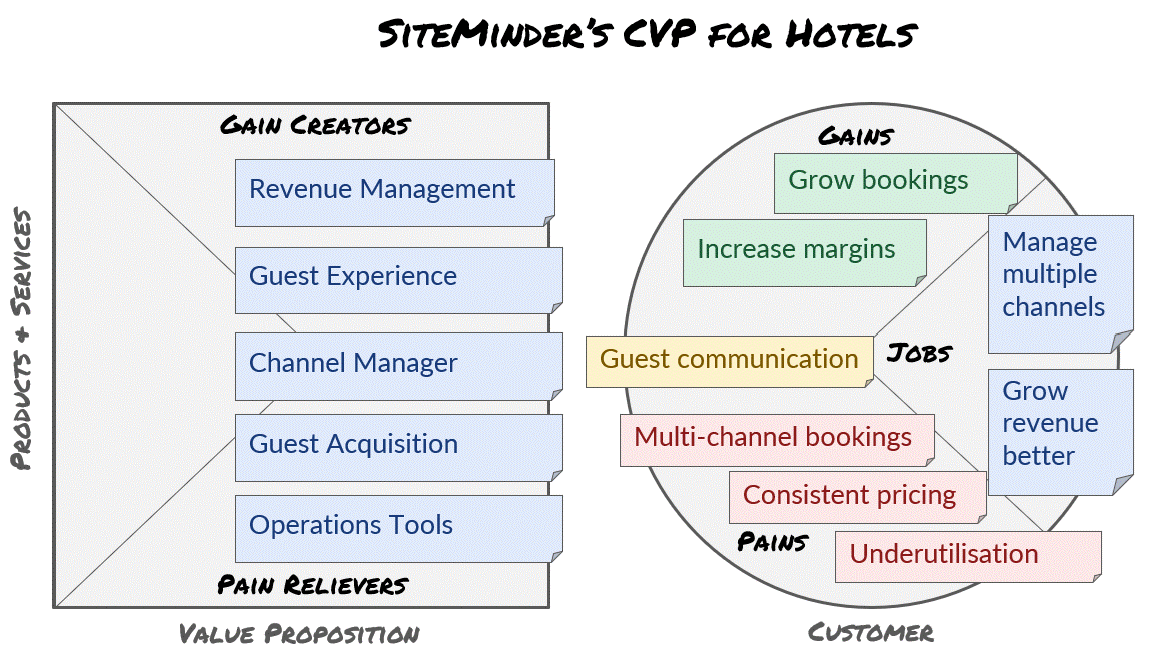

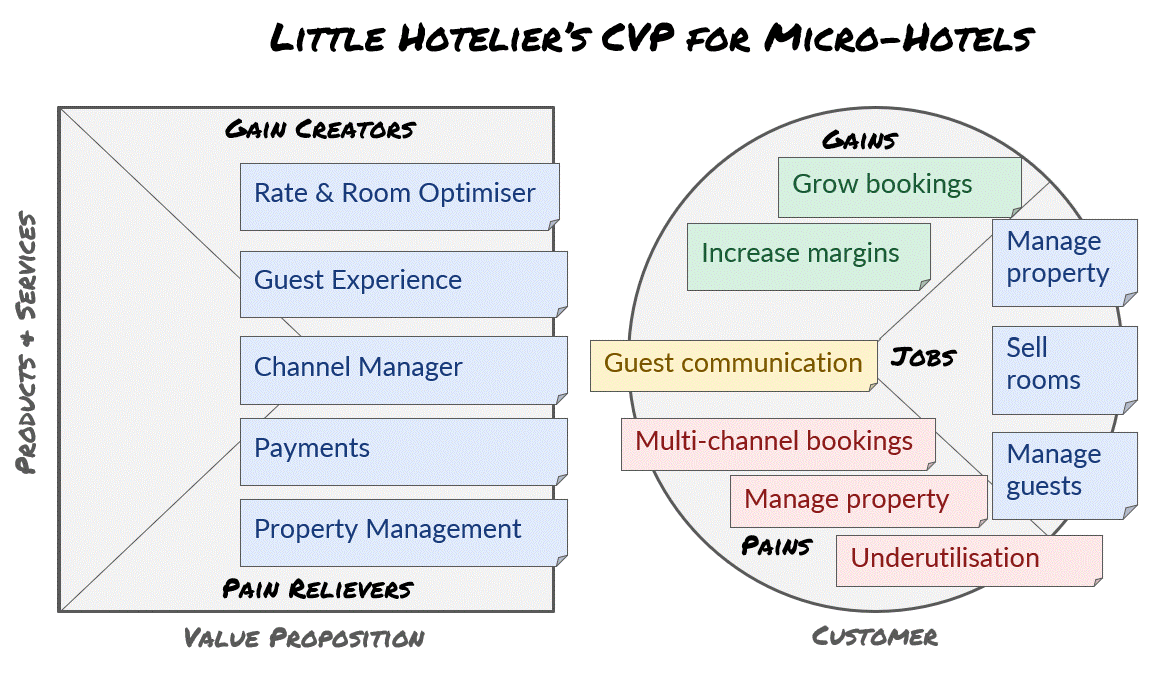

Customer Value Proposition

SiteMinder’s core value proposition is to help mid-sized accommodation providers publish, synchronise and optimise their inventory across multiple channels. These providers typically have various hotel management systems in place (the industry calls them the PMS, CRS and other acronyms). Here is the CVP canvas:

SiteMinder is increasingly focused on winning larger hotels and hotel chains (as per recent public reports). This takes direct sales effort and product improvements, like the operational tools and connections to proprietary hotel management systems.

Without SiteMinder or a product like it, the hotel is going to need to be checking each channel they are listed through and updating availability and pricing in each of them every time a booking comes through. This is almost impossible with 10 rooms, let alone if you have over 100.

The hassle involved in updating the dozens if not hundreds of channels you could publish your rooms to, then keeping this up-to-date makes the core value proposition of SiteMinder compelling. Layering in products and features to help optimise and grow revenue further strengthens this value of the product.

Little Hotelier handles a wider variety of tasks for a micro-hotel but does so in a simpler way.

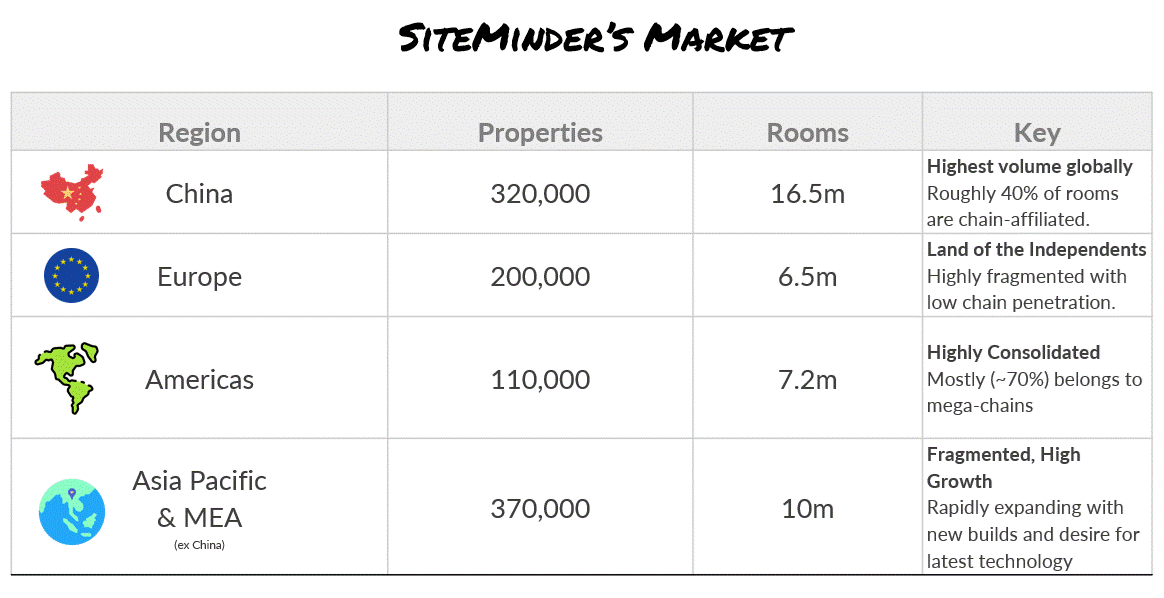

Market: Room To Grow

There are two parts to SiteMinder’s market. One is the accommodation providers globally and the other, because of the transaction revenue, is consumer demand for accommodation.

Accommodation Providers

The broad market for SiteMinder is any hotel or accommodation globally. This can be segmented by geographical region and by size.

The chart below shows how the market breaks down by different regions and their different characteristics:

Sources: Eurostat, American Hotel & Lodging Association, Chinese Government, HVS and others

The global market can also be sliced by size of accommodation:

Small Properties (1-20 rooms): B&Bs, vacation rentals and tiny boutique hotels. This is the sweet spot for Little Hotelier but the the SiteMinder Channel Manager can also integrate with another PMS they might have.

Midscale (20-100+ rooms): independent hotels, regional chains and mid-market groups. This is SiteMinder’s core as they have enough rooms to need automated distribution but aren’t necessarily large enough to invest in building their own systems.

Large Groups: large international hotel chains. The large groups have historically built their own systems or used large vendors like Amadeus or Oracle for centralised systems. This is the market SiteMinder appears to be now pursuing more aggressively.

Most of the global market is accessible to SiteMinder given (a) its presence across the globe and (b) historical and recent success with smaller properties, independents, fragmented markets and non-chain affiliated hotels.

The future market of larger chains is where SiteMinder appears to be gaining ground. It will be interesting to see how far they can get here as it opens up an even bigger serviceable market for them.

Consumer Demand for Travel

Consumer demand for travel matters for SiteMinder because it will impact their Transactional Revenue, especially as this becomes a greater and greater share of their overall revenue.

Generally speaking, there are two parts to consumer travel demand. Business travel and personal travel.

In personal travel the key trends are:

Macro Growth: Consumer demand for leisure travel remains highly resilient, with the sector’s global GDP projected to grow faster than the broader economy (World Travel & Tourism Council in May 2026, so after many of the shocks from earlier in the year). Even where the cost of living is having an impact, people are taking shorter, more local travel (U.S. Travel Association, May 2026).

Grey Travellers: Affluent seniors are a growing and seemingly resilient group. A high proportion of over 50s feel comfortable spending retirement savings on travel and, as a result, twice as many went on a major holiday in 2025 as compared to 2022. The vast majority (68%) are using their savings, making them potentially more resilient to macroeconomic conditions (see the Grey Gap Year Report). (The numbers are for Australia so I’m assuming similar countries have the same trend to extrapolate globally)

More Digital, Not Less: Gen Z and Millennials represent around half of all active travellers who are now seeking more experiential, digitally integrated trip planning (Deloitte, 2026). AI might drive even more of a need for accommodation to increase its digital capabilities and integrations.

In business travel, the trends are:

Purpose-driven travel: Most businesses are more focused on travel for a genuine purpose compared to pre-COVID when less scrutiny or justification was required. So, once adjusted for inflation, business travel spending still remains below pre-pandemic peaks (Quantum Run analysis of multiple reports).

Corporate travel buyers view AI as critical: Businesses are increasingly looking to AI to help corporate travel buyers optimise, understand and plan travel better (Global Business Travel Association, April 2026).

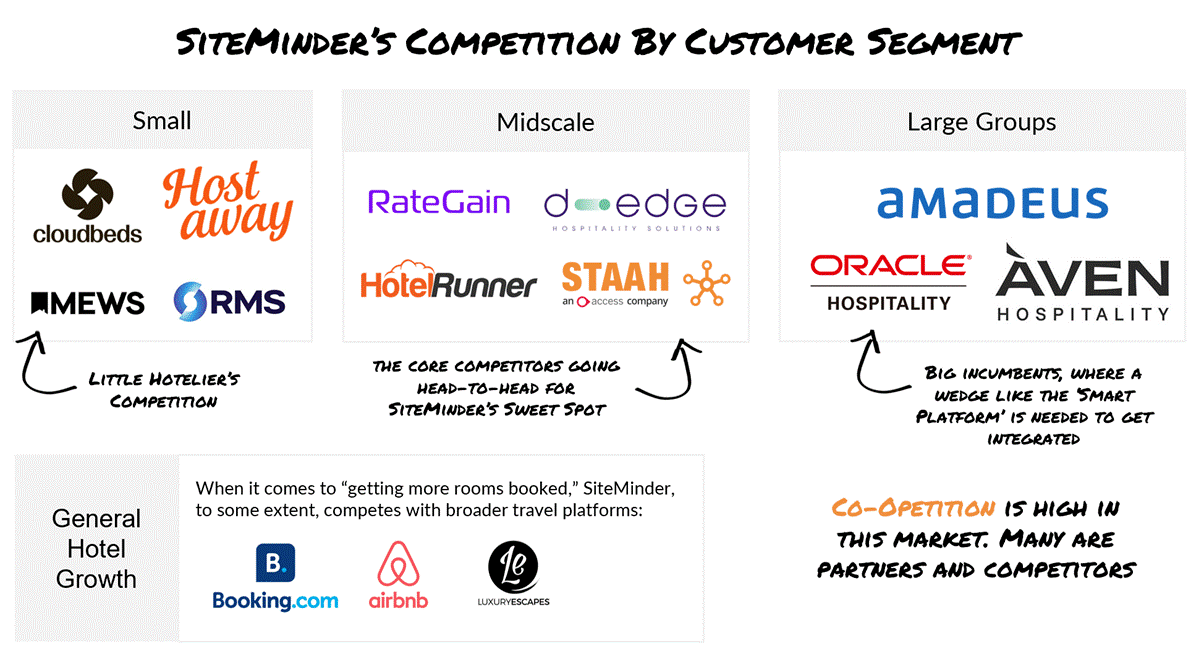

Competition: Or Co-Opetition?

The competition for SiteMinder, segmented by size:

A few callouts on competition:

Of the Midscale, Direct Competitors: the ones sampled all had fewer customers than SiteMinder. Those in the chart above had 10,000 to 30,000 customers each.

Big Enterprise Gorillas: the big systems – like Oracle, Amadeus and Aven (formerly Sabre) are all centred around large-scale implementation and integration across other systems like ERPs, ticketing and more. The switching cost is high, but customers are often looking for more nimble, leading edge partners to work with alongside their big, slow moving system.

Co-opetition: In the small end of the market, many of the property management system companies (like RMS and Mews) are partners as much as they are competitors. SiteMinder integrates with many of them and recently announced that its product will be embedded within Mews.

Go-to-Market: Standard SaaS Mix

SiteMinder has a typical marketing mix for a software-as-a-service business of its scale.

The different Go-to-Market motions that SiteMinder uses are:

Event Sponsorship: having a presence at key travel conferences

Partnerships: integrations and reseller agreements with complementary software and marketing agencies

Digital Ads: paid advertising online to capture demand

Review Sites: being listed and reviewed in sites like HotelTechReport and G2Crowd. Customers, particularly smaller ones, often use these as a key part of a buying decision

Direct Sales: salespeople proactively working to win accounts.

Upsell: sell the add-ons to the existing customer base.

The highly scalable, low cost go-to-market channels (Partnerships, Ads, Review Sites) are critically important for SiteMinder because of the economics. With average revenue per user (ARPU) of ~$435 and lifetime-value (LTV) of $31,108 (H1FY26 release), there is only so much spend you can do to acquire a customer. This is especially true for Little Hotelier with what is likely to be an even lower LTV.

SiteMinder is currently operating well within these bounds, spending an average of $4,447 to acquire a customer (CAC). There is room to be more aggressive if they wanted to be.

On aggressiveness, SiteMinder has stated that they are working to win larger customers now. This escapes the current unit economics in that a large hotel chain likely has an LTV of hundreds of thousands or millions so you can afford to allocate a dedicated sales person to a small number of high value targets. It’s worth watching how this plays out and why I love segmented metrics more so than averages.

Lastly, the Upsell is a significant opportunity. A minority of their customers use their new add-ons. There is a huge opportunity just adding their new add-ons to existing customers. Their customers get more value and SiteMinder earns more per customer.

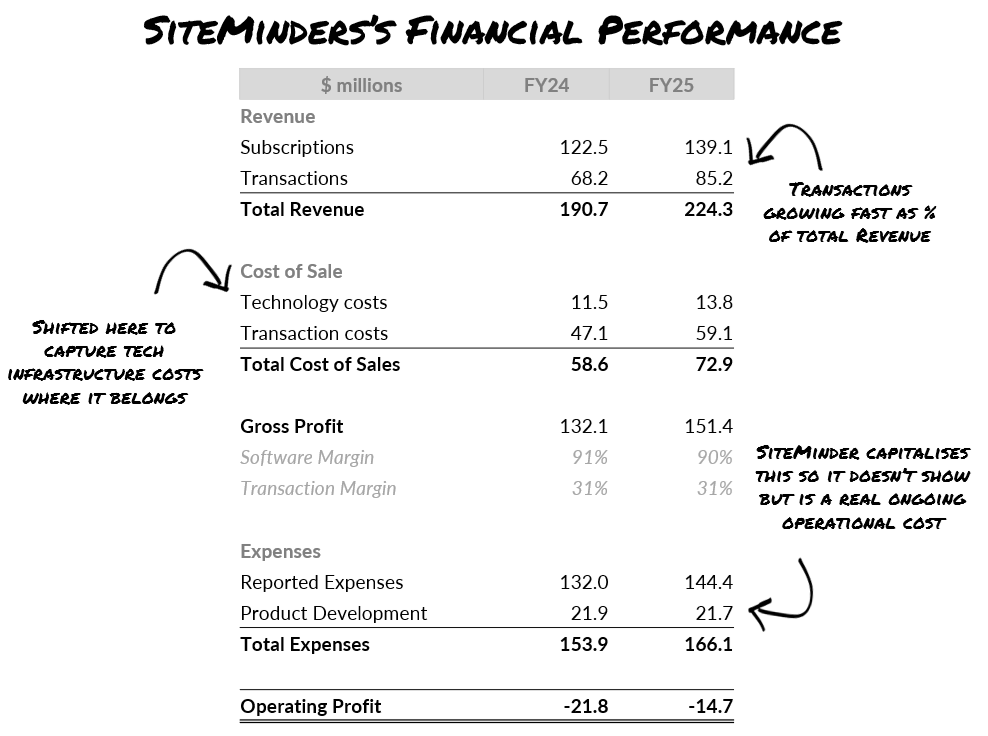

Finances: To Profit Or Not To Profit

SiteMinder has been growing consistently ~22% year on year, on average, over the last 5 years. Over the last three years it’s been doing this at or close to cashflow break even, but making losses.

The most recent full year financials are below. The costs are adjusted from what the company reports in order to arrive at a stronger representation of Operating Profit.

The key points on SiteMinder’s financials are:

Product Development Costs: SiteMinder capitalises their R&D. There are reasons for why this is a good thing and their reporting of it is inline with accounting practices. However, accounting practices don’t help us understand the operating economics of the business so we need to bring this back in. Product Development is unarguably an essential part of business-as-usual costs for any software company.

Transactional Revenue: Throughout SiteMinder’s reports they talk about Transactional Revenue being “ARR” (Annually Recurring Revenue). Later in their most recent report it gives definitions for how this revenue is recognised and it is tied to outcomes for their customers (like commissions on bookings, % of payments). This isn’t annually recurring revenue. It’s very much, by their own definition, variable revenue. It could fluctuate substantially per customer, by season and by customer demand.

Transactional Margin: The transactional margins are substantially lower than SiteMinder’s good old fashioned software subscriptions. For SiteMinder, especially in the age of AI, the transactional products add defensibility to the core and give the business access to additional revenue without too much additional acquisition spend. It’s lower margin but needs to be viewed as accretive to the whole and adding defensibility.

Key Risks

The key existential risks to SiteMinder are:

Travel disruption: A major shock to travel could significantly impact revenue, especially now that transaction revenue is becoming a greater portion of the group’s income. SiteMinder has shown its subscriptions can weather a major travel shock like COVID and the end-customer outlook for travel seems promising. However, the travel disruption risk can’t be completely ignored or written off.

AI: AI and AI-driven travel agents are a hot topic. AI could, in theory, automatically seek out and interact with hotels directly and bypass SiteMinder and its integration partners. While it is theoretically possible to envisage this world, in reality a system like SiteMinder that has handled the integrations to give AI the interface probably becomes more valuable, not less.

Growth v Profitability: The company is walking a middle line between exceptional growth and (genuine) profitable growth. It’s not clear how the market will view this in the long run and where the company will run in the future. By not picking a clear lane, especially in the post-SaaSpocalypse era, it may create problems for shareholders and management.

Key Scenarios

The Key Scenarios for SiteMinder are likely:

1. Current Trends Continue: the current market conditions remain similar and SiteMinder continues its revenue growth, probably with some acceleration as transactional products are attached to more and more of their existing base.

2. Travel Headwinds: one of the many geopolitical issues going on (or even a new one) means travel is interrupted. This would likely be measured in months or years but temporary.

3. Large Group Sales Accelerate: SiteMinder’s new platform and investment in selling to larger groups leads to bigger contracts and faster growth. In an even more bullish scenario, you could see SiteMinder’s traditional, midscale target segment buying faster or moving from competitors if the new, smart platform is genuinely good.

Valuation

The Margin of Safety valuation is the best starting point, giving you a firm base to then workout how much risk, if any, we want to take.

Likely Case

In the short to medium term, there is a strong argument to say the Current Trends Continue is the most likely case. Under this case, if we hold costs constant and the current growth continues, then we get to about $282m in revenue and an Operating Profit of $21m sometime during calendar year 2026 or at least by FY27.

The key variable on the profit is what management intends. Whether they intend to keep running at cash flow break even to reinvest in growth or whether they are going to build profitability.

All of the Operating Profit will likely come from revenue growth on the assumption costs remain about the same. There is a chance costs are rising because hiring is on an upward trend at SiteMinder, but let’s ignore that as it’s hopefully immaterial.

This means the current valuation of A$1.1B is around 53x near-term Operating Profit or 3.9x revenue. This has jumped from 38x when I started this analysis 2-3 weeks ago.

Travel Headwinds

If something disrupts travel in the short-to-medium term then transactional revenue growth is likely to stall and overall revenue may even take a small step back. Given profitability is mostly going to come from revenue growth, profitability will likely not occur or be $20m-$40m losses.

In this scenario the current valuation is steep, leaving little margin of safety.

Large Group Sales Accelerate

If SiteMinder’s new offering services larger groups better, then revenue could grow further or at least continue on or around current rates for a while into the future.

This scenario makes the revenue multiple valuation look relatively low. However, viewed through the lens of (potential) profitability, growth like this is being increasingly priced in as the share price climbs.

Closing Thoughts

SiteMinder was probably unfairly devalued by the SaaSpocalypse but we can’t forget the possible disruption to global travel that was happening around the same time. It’s hard to pick these two influences apart from the decline in valuation.

The business continues to post growth and is able to do so under its own cashflow.

SiteMinder’s strong, global market position means it is well-placed to continue growing. Its transactional offering and hundreds of integrations give it a moat against artificial intelligence eating its lunch.

The big challenge facing the business is figuring out where it wants to sit on the growth versus profitability curve, particularly with how capital markets are shifting their thinking on software businesses. It will be interesting to watch whether profitability starts playing more into the focus for the business.