Mopoke Cloud Index 2025

ASX-listed, high potential technology companies

Here is the 5th annual update for the Mopoke Cloud Index.

That’s right, we’ve been tracking promising ASX tech companies for 5 years now.

We use our Mopoke Cloud Index as a framework to identify technology companies with high potential that are worth deep-diving into.

What companies are we looking for?

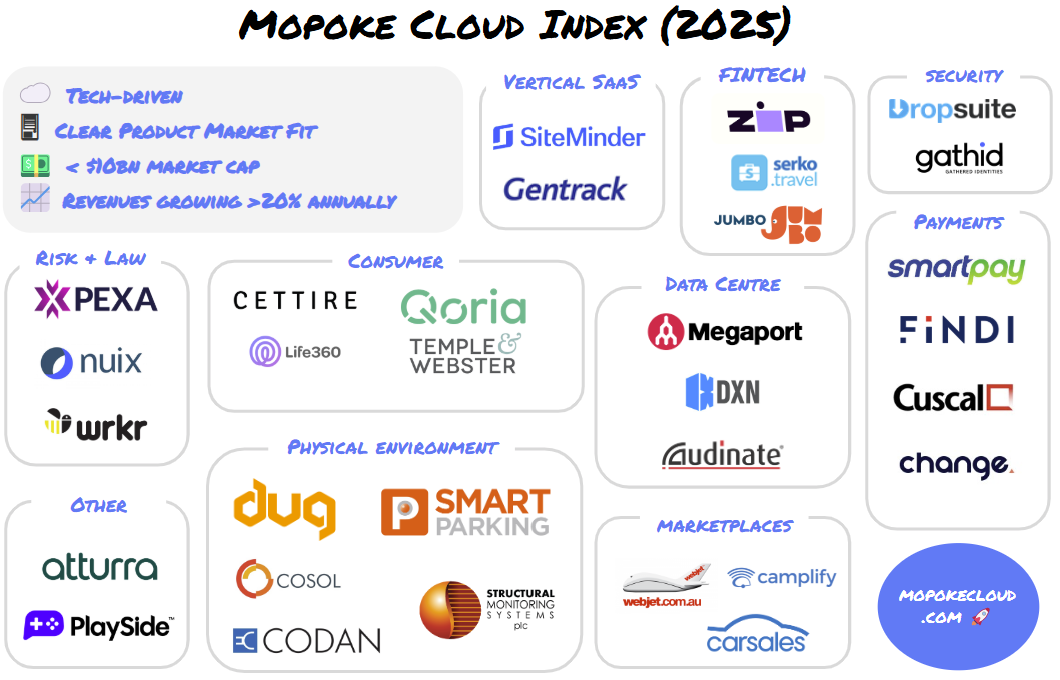

For the Index, we look at the 180+ technology companies listed on the ASX and then select a subset with the following characteristics:

☁️ Software or cloud-based products: this may seem like a moot point, but much of what is defined as ‘technology’ on the ASX isn’t necessarily software, but can be things like hardware or technology services. We want to focus solely on software products with high gross margins and scalability.

🖥 Clear Product Market Fit (PMF): the company has built a software product or service that sells - typically because it is cheaper, faster or better than existing solutions. The real test of PMF is unit economics which we’ll be digging into in another post, but PMF can be time-consuming to assess and few companies will tell investors that they don't have product market fit. To keep things simple, we define PMF as having greater than $10m of expected revenue in the next twelve months (NTM).

💵 <$10bn market cap: the best investment opportunities are likely under-followed by brokers and institutions, and the law of large numbers is difficult to escape. We want to increase our chances of finding companies that could grow to be 10x bigger in the next few years.

📈 Revenues growing >20% annually: technology investing is mainly focused on growth, so we want to find companies with momentum (normalizing for any COVID-related disruptions).

Why we do this?

Australia’s public technology companies provide a window into what’s happening in Australia and globally - many of our businesses play in global markets. It helps us see what’s working, where opportunities are and, hopefully, we might find a good investment.

Mopoke Cloud Index 2025

Insights

In putting together the index there are a few observations worth sharing:

15 less companies: In 2024 there were 46 companies that met our performance criteria, this year in 2025 there are only 31. That’s a loss of 15 companies. Some were acquired, like TASK, and some grew beyond our $10bn market cap, like Pro Medicus, but many didn’t meet the performance criteria.

Less categories: the loss of companies meant it wasn’t worth breaking the companies into as many categories. We dropped Sales & Marketing and Games, both are industries that anecdotally seem to have been under pressure.

Emerging categories: We introduced two categories: Physical Environment and Data Centre. With AI, Data Centers and related services are gaining more and more momentum. Physical Environment is an interesting one to emerge, the meeting point of software and hardware working together to digitally transform physical industries.

Only 2 ‘pure’ vertical market SaaS - as an area we invest in, it was interesting to observe that only two pure-play Vertical Market SaaS companies, Siteminder and Gentrack made the criteria.

Cost of living? Temple & Webster unexpectedly made the list given the general sense of cost of living pressure.

What next

Subscribe to get deep dive analysis on the companies in the index, insights around trends shaping the index, insights into tech companies and more.

Thanks Scott, if the index was a portfolio what would be the 1year and 3 year performance?