Four Profiles of AI Durability on the ASX

Small-cap SaaSpocalyse Survivors on the ASX

26 ASX-listed tech companies bucked the February 2026 SaaSpocalypse despite having seemingly limited AI moats.

Some just held their value, some had made meaningful gains, while a small number produced exceptional returns.

These mostly smaller-cap companies provide an interesting window into what the market thinks durability looks like for tech in the face of AI.

This article, the fourth in a series on AI durability and ASX tech, looks at four company profiles that emerge from analysing share price, performance and moats.

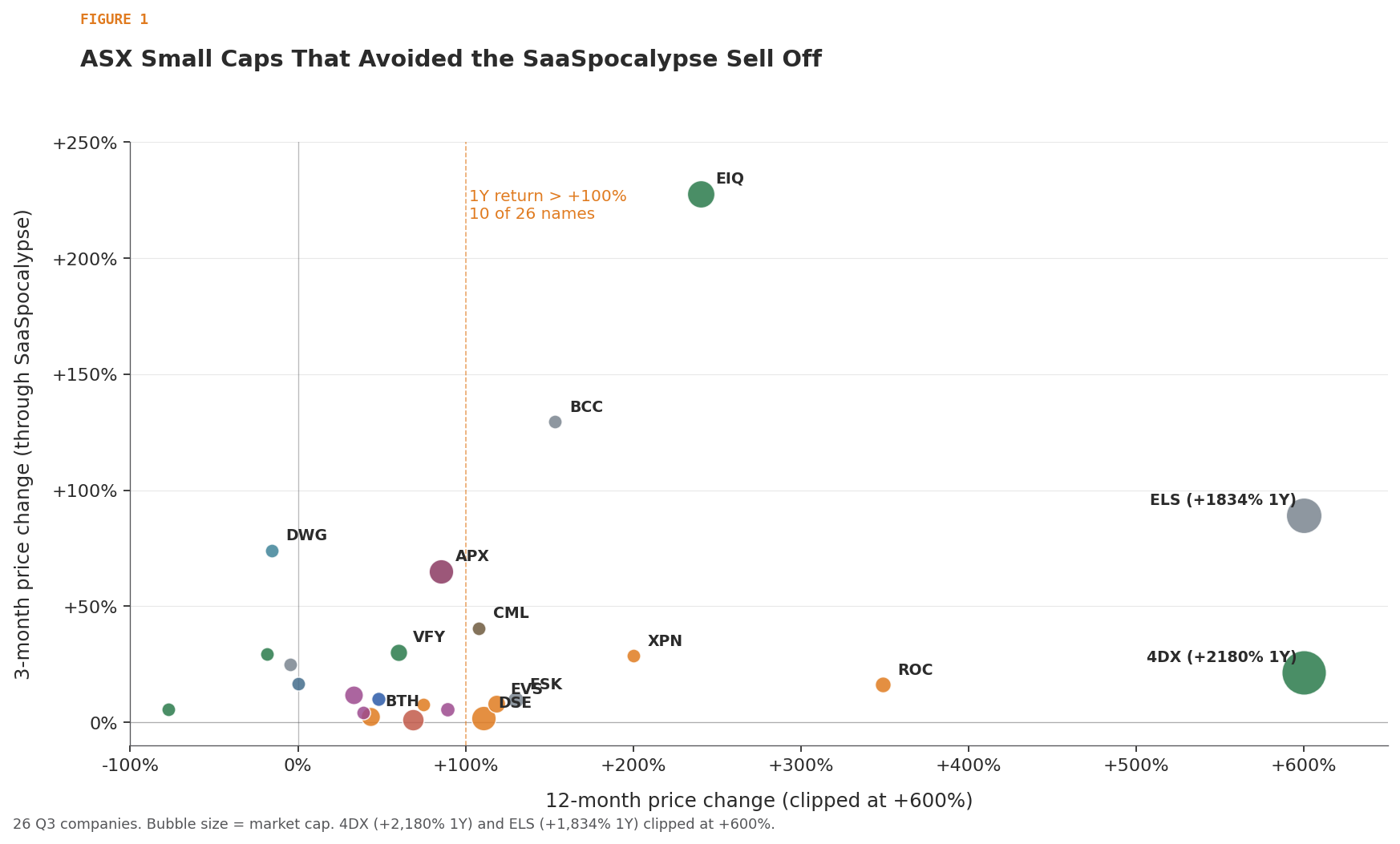

Figure 1. The 26 ASX-listed tech companies that bucked the February 2026 selloff, plotted on 1-year price change against revenue growth. Coloured names have at least one moat scored 2+ on the AI Moat framework.

Durability Profiles

Strip the noise: M&A

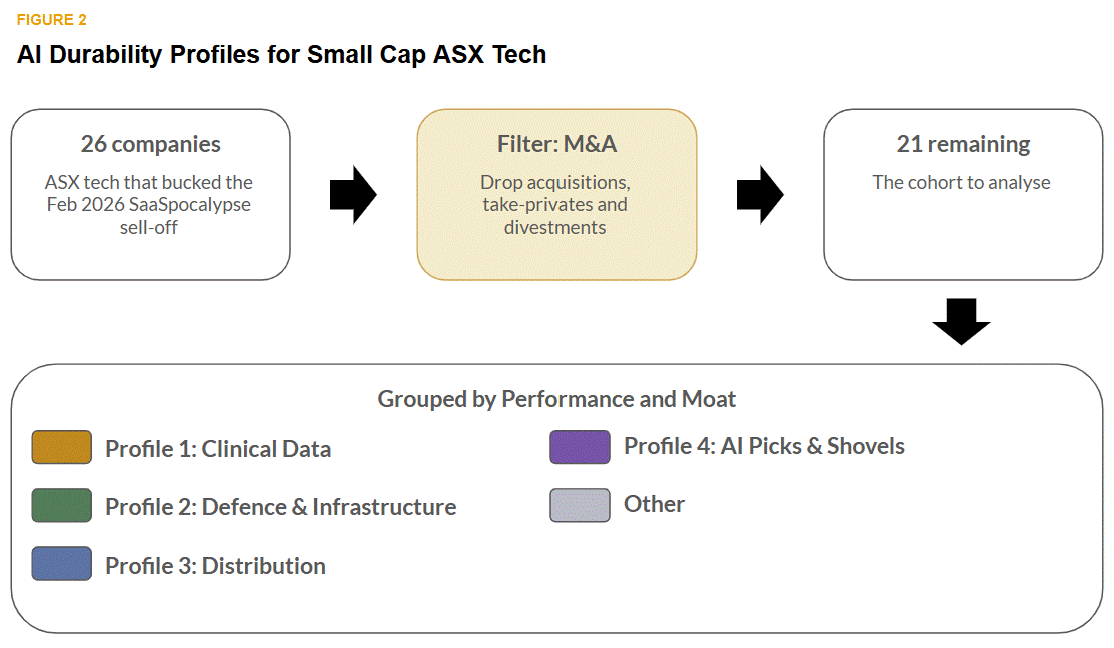

Before we can draw out profiles from this cohort of companies, we need to clear out some noise from M&A. We will filter out companies that have announced take-privates, acquisition bids, or significant asset sales (DSE, BTH, EVS, MPA, BCC). These are currently trading more in relation to the deal price rather than a market view on the durability of the business. Once we drop these, we are left with 21 companies.

Figure 2. The M&A filter and the five groupings the cohort sorts into.

The 21 remaining companies were sorted into Profiles by contemplating the moats, sector, customer profile and operating data:

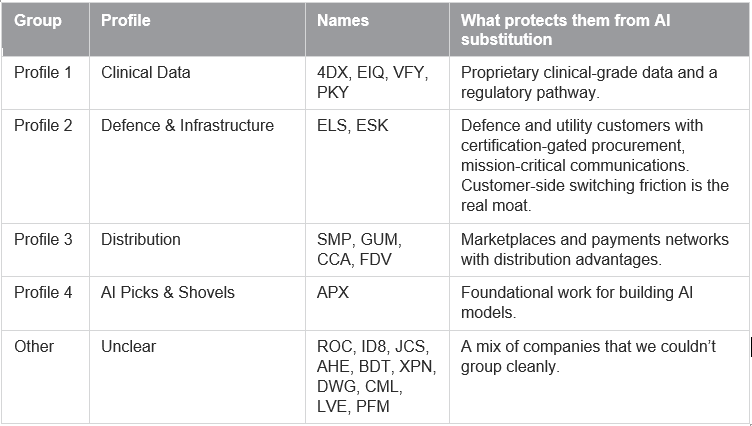

Table 1. Grouping the companies by common attributes.

The rest of the article defines the four profiles, then shares charts and analysis on them.

Profile 1: Clinical Data

These companies have clinical data and regulatory protection, and the two combine to compound.

The companies are:

4DMedical: has FDA clearance plus multi-jurisdiction approvals and proprietary clinical imaging data.

Echo IQ: 24 years of cardiac imaging.

Vitrafy Life Sciences: cryopreservation technology with hardware, regulation and data coming together.

Pathkey: An AI pathology company that is still developing its moats in proprietary clinical data and regulation.

Clinical-trial-grade data is a hard data set to acquire and hard to develop intelligence around, given the focus on health and safety.

Revenue and profitability performance are at emerging-company stages. All four are EBITDA-negative. 4DMedical is at +56% revenue growth on a A$3.9M base; Echo IQ is essentially pre-revenue, Vitrafy’s revenue declined -49%, and Pathkey’s revenue declined -65%.

Given fundamental performance can’t explain this alone, the market appears to have recognised this as a tough form of AI durability. (or maybe they’re punting?)

Profile 2: Defence & Critical Infrastructure

These companies provide technology for defence with a strong hardware focus.

The two companies are:

Elsight: connectivity solution (hardware and software) for drones on the battlefield or in similarly sensitive environments.

Etherstack: software for wireless communication in highly sensitive environments like defence and critical infrastructure (i.e. utilities).

The moat here is around the nature of the solutions and their customers. Defence and defence-like solutions tend to have higher switching costs, are deeply embedded in workflows, and involve data that is hard to get. For Elsight the physical aspects of the hardware components of their solution adds further defensibility.

Financially, they’re posting small profits or breaking even. Both are growing in revenue.

Profile 3: Distribution

These four companies have network effects, distribution moats or a bit of both, all underpinned by profitability.

The companies are:

Gumtree: classifieds marketplaces, running profitably.

Smartpay: payment terminals, running profitably.

Change Financial: card issuer, around breakeven but growing quickly.

Frontier Digital Ventures: partner to build online marketplaces, around breakeven.

The network effects of marketplaces and the distribution channels of payment terminals are difficult for AI to challenge.

Profile 4: AI Picks & Shovels

Appen gets its own profile. Appen is the only company in the broader cohort directly participating in the foundational work behind the large-language models. The picks and shovels of the gold rush if you will.

On the 8 AI Moats Framework Appen scores well on the Data and Scale moats with 1M+ people doing annotations for them across 235 languages to help train some of the leading AI models globally.

The genuine durability question is whether the moat survives when the buyers of training data (foundation model labs) are themselves the substitution threat.

Analysis of the Durability Profiles

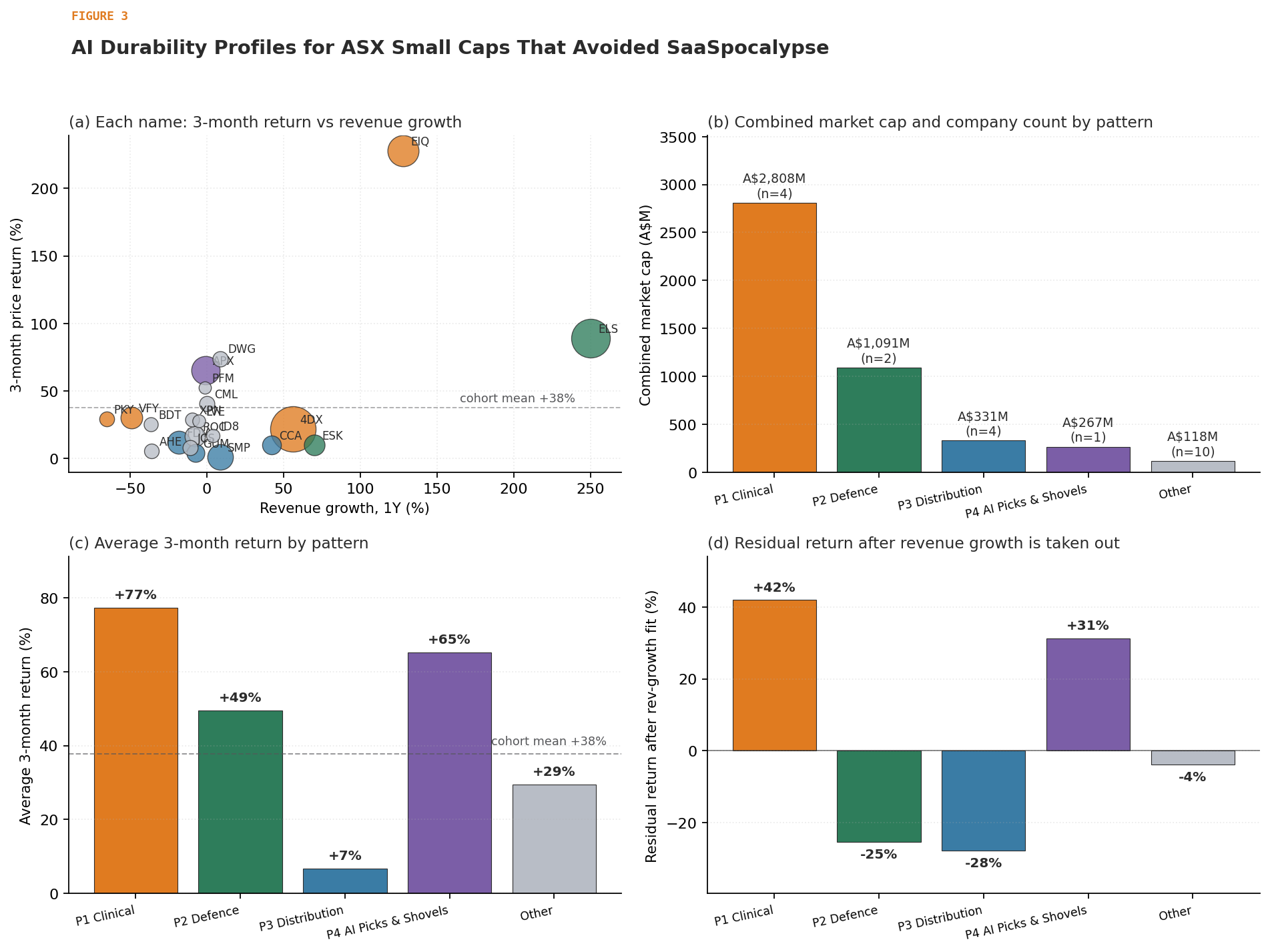

Now that we’ve defined a few profiles, we can do some analysis to understand them further. The chart below looks at some key metrics of the Durability Profiles:

Figure 3. Comparison of Durability Profiles. (a) Each name plotted on 3-month return against revenue growth, bubble = market cap. (b) Combined market cap and company count per profile. (c) Average 3-month return per profile, against the cohort average of +38%. (d) Residual return per profile after a simple linear fit on revenue growth (a proxy for the market’s view on AI durability separated from operating performance).

This next chart looks at the Durability Profiles, their profitability, revenue growth, and returns:

Figure 4. The companies plotted on revenue growth (X) and EBITDA (Y), with bubble size/shape for returns and colour for profile. ELS would be off the chart at +1,024% revenue growth.

There are a few observations that come from these charts:

Revenue growth, more than moats and EBITDA, shows a strong relationship with returns. Arguably, this is stronger than moats or the Durability Profiles. But, they’re also somewhat related (strong moats drive revenue growth and growth lets you build moats). In the long tail of other companies this appears to be the primary driver of share price.

The Durability Profiles do appear to hold up with the market’s view. Each profile had a positive relationship with returns during the SaaSpocalypse. We would need to test it across a broader sample size to draw bigger conclusions. But on the surface these are logically durable businesses in the face of AI.

Power Law: The charts show two companies really carrying a significant amount of the weight of returns and performance. This likely skews the significance of the durability profiles as well.

Absence of certain profiles: as much as what shows with the profiles is what is missing. The much previously hyped typical SaaS workflow/data moat type of profile doesn’t show up.

AI and the ASX Series

There is still more to come in this series on the SaaSpocalypse, AI and ASX technology companies. You can read previous articles in the series here: