Appen: the $309m fall in AI revenue

How segmenting between AI Builders and AI Adopters might help it return to growth

Being at the forefront of AI isn’t a straightforward ticket to rocket-ship growth. Appen, an AI data annotation company listed on the ASX, is going through some severe performance issues.

Appen has gone from profitable with growing revenue to declining revenue and losses. To add salt to the wound, Google recently ended an $82m contract.

But, through analysing Appen and the forces at play in AI, it looks like there might be a segment of the business that has a high gross margin, probably growing and supported by strong tailwinds.

This hidden segment, data annotation for the AI Adopters, is obscured by the significant revenues Appen gets from massive technology companies like Amazon, Facebook and Google.

The AI Adopters segment is only 29% of total revenue, but its gross margin is 38% of the overall margin.

Appen needs to navigate servicing large contracts with the world’s biggest technology companies while quickly growing into the market for companies adopting AI. They’ve just raised ~$30m in working capital to help them start to figure this out.

If they can’t figure it out then they’ll need to either take drastic action or sell the company to someone that can take on the turnaround.

It’s an intriguing situation. Let’s take a closer look at Appen.

About Appen

Linguist Dr Julie Vonwiller founded Appen in 1996 with her engineer husband, Chirs Vonwiller.

In 2009, Anacacia Capital acquired a 51% share of Appen as the Vonwillers looked to transition out and retire. Over the next 18 months, Appen increased its holding to 70% for a total investment of $5.5m.

Appen was then merged with the Butler Hill Group, a US-based firm with a similar offering to Appen. The Butler Hill Group was founded in 1993 by ex-IBM Watson researcher Lisa Braden-Harder.

The merged group was IPO’d in 2015, led by Braden-Harder.

Appen went on to make a handful of acquisitions: Wikman Remer, Mendip Media Group, Leapforce for $80m USD, Figure Eight for $300m USD and Quadrant for $45m.

Appen’s stock price surged but has fallen in line with falling revenues and losses. Appen recently raised a $30m round to help fund working capital to ensure the business survives.

Product (or Solution): A workforce for tagging AI, supported by specialised data and software

Appen’s solution is about tagging and reviewing data used in AI and Machine Learning.

It’s primarily a large army of people working away to tag, review, edit, and markup data to feed into algorithms or that has come out of algorithms. These people are made more efficient and effective by Appen’s technology and prebuilt data sets.

Source: FY21 Annual Report

The key features of Appen’s solution are:

Ready to go data sets to help train, tune or validate AI. Like data sets for domains like health care, finance and vehicles.

The Crowd (the people) to build data, prepare data and evaluate results. These can be relatively unskilled or trained copywriters/linguists.

Software to make data preparation, sourcing and evaluation better. Including algorithms to automatically fix data, make tagging easier and prefill.

Management of the people, software and data to make this efficient and effective. Including hiring the people, determining pay, scheduling them and training them.

Business Model:

Appen’s business model boils down to:

A Salesperson sells a project for an average size of $120,000 (as per annual report)

The Crowd works it (i.e. tags, labels, evaluates), Appen’s technology helps the client and the crowd.

Appen makes a Gross Margin of ~38% (as per annual report)

Client (might) do repeat projects, especially with some Account Management. This could expand to millions in revenue.

Reinvest the margin in better ways to help build, prepare and evaluate AI data.

Appen has had some substantial customers (Facebook, Google, Microsoft) who have been in the repeat projects loop with substantially larger-than-average projects. For example, Google did $82.8 million with Appen in FY2023. But these massive customers are falling away.

Market: the challenge and opportunity of being on the edge of AI

The market for Appen is interesting in how rapidly it is evolving and how turbulent markets at the forefront of technology can be.

Appen is primarily in the now fairly competitive ‘data annotation market’ and, to some extent, the crowd-sourcing market with a specialism in AI. Both markets are estimated to each be $4-$5 billion markets that are growing.

Companies in annotation, like Snorkel AI, reported a five times increase in enquiries in late November 2023.

What’s happening in AI?

Everything AI-related is undergoing a significant shift due to recent innovation.

The most well-known is the explosion of large language models like OpenAI’s ChatGPT.

However, behind the scenes, progress has been made by cloud vendors and data platform providers. They are looking to commoditise and give greater access to the tooling and infrastructure required to configure and run artificial intelligence and machine learning.

In some cases, especially in the larger or more AI-focused tech companies, algorithms have been built to help annotate and label faster.

Algorithms need data, and lots of it, to be developed. Then, once developed, they need to be tuned from time to time with more data.

We do have large, open annotated data sets for images (e.g. ImageNet), speech (e.g. the 10 data sets on Stanford’s website), and language. There is also a much larger trove of data within Amazon, Google, Microsoft, OpenAI and others (including Appen). Amazon, for example, has hours of recordings from people talking to Alexa.

But, we haven’t yet built “The Final Algorithm”. So, this process of annotating large data sets, training AI on it, and then tuning it is likely to continue for some time.

The building of new algorithms, generally, requires volumes of new data that is annotated and output that is evaluated. This needs large data sets to be labelled that haven’t been labelled or annotated before in the way you need.

Adapting these algorithms, which is what most organisations applying AI are doing, is where you tune or customise algorithms to your specific requirements.

Appen’s Market Segments: Adopters,Builders, and Users

This broadly means the market for Appen breaks into these segments:

AI Builders: the companies building new algorithms such as Google, OpenAI and Microsoft, as well as more specialised technology companies.

AI Adopters: companies looking to customise what the AI Builders have created for their own uses.

AI Users: companies that will use the AI and algorithms others create without any modification.

The AI Builders will continue to need to build algorithms. So they will continue to need labelled data, and they will continue to need to evaluate their algorithms’ output.

The key questions for this segment are:

Have the major data sets been mostly annotated (for now)? The AI Builders have possibly performed the bulk of annotation for datasets around image, language, and speech. If so, it’s into tuning mode (less need for annotation).

Is there another major data set or algorithm on the horizon? If so, what element of human intelligence would it be? If there is, then there will be another massive need for annotation and data preparation.

Do the algorithms they’ve developed now allow their AI to annotate and evaluate itself? If this is even partly correct, then the need for humans in the loop has decreased (Appen’s loss of Google might be a sign of this).

The AI Adopters are currently working to apply the recent advances made by the AI Builders. This requires data, data annotation and labelling but not at the same scale as building AI models.

The AI Users don’t require any data annotation services. Most small to medium businesses will be AI users. Larger businesses may be AI Adopters in one department (where it gives a competitive advantage) and AI Users in another where it provides no real advantage (i.e. payroll for most).

The number of AI Adopters is large; almost every meaningfully sized company on the planet is arguably in this market. While the number of AI Builders is small: in the tens, maybe hundreds.

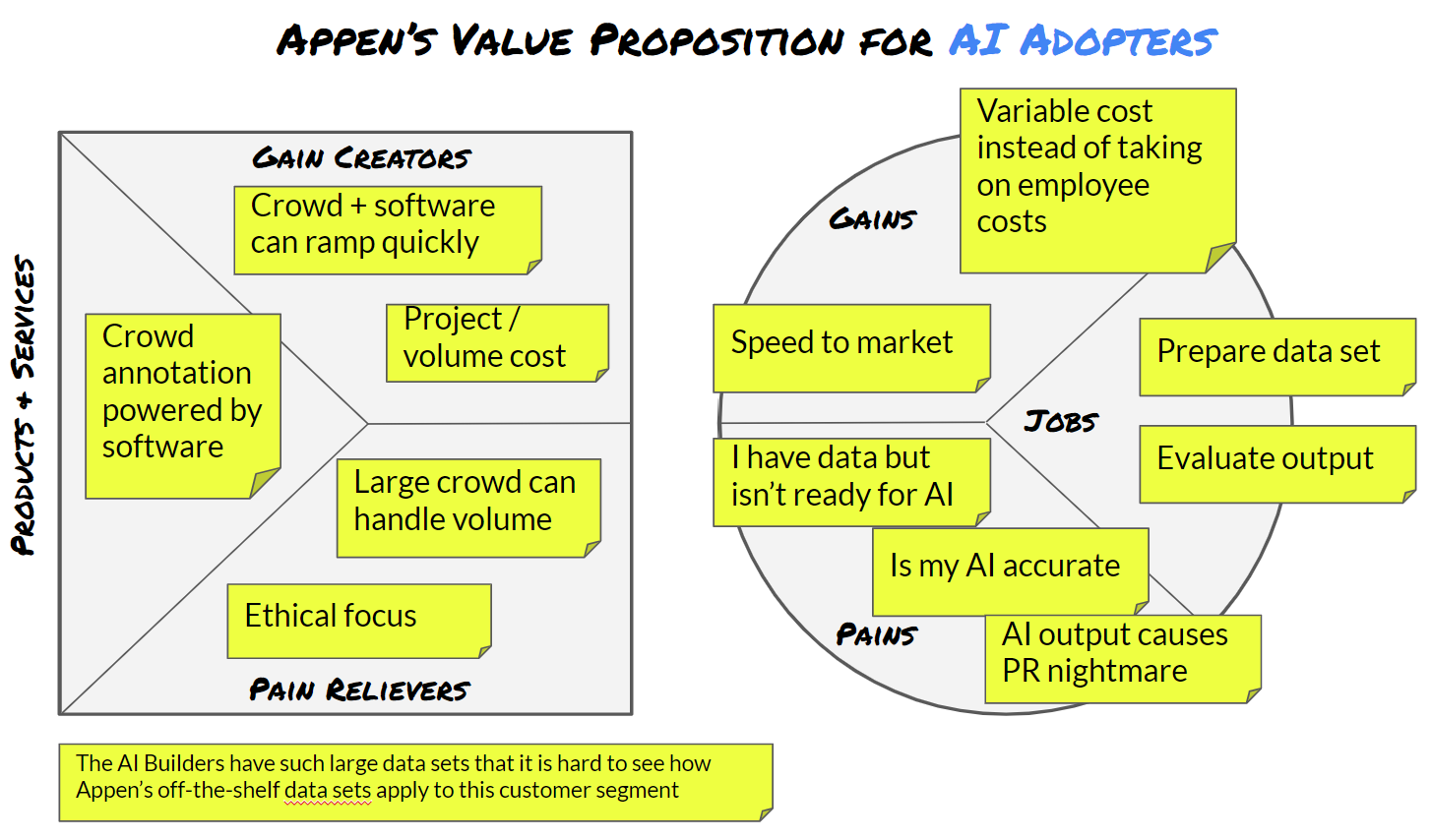

Customer Value Proposition

The Customer Value Proposition (or CVP) differs for the AI Builders and AI Adopters. We won’t cover AI Users because they don’t have a need for annotation.

AI Builders

AI Adopters

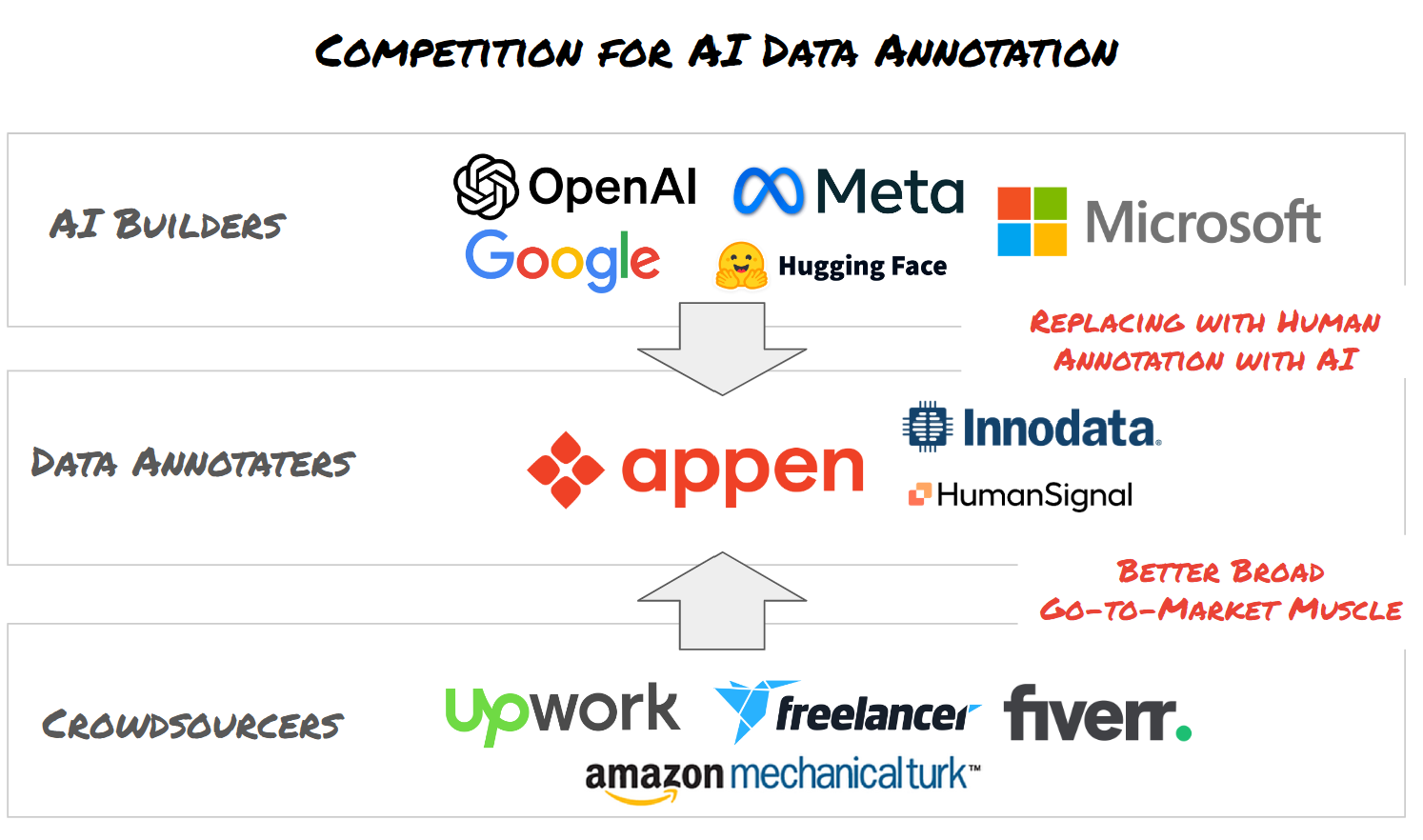

Competition: Pressure from big customers and marketing machines

Appen’s competition comes from other Data Annotation Solutions, Crowdsourcing more broadly, and the AI Builders themselves creating better Annotation AI.

Companies providing Data Annotation Solutions provide a fairly similar offering to Appen. They help prepare data and evaluate algorithm output with teams of people and software to help manage this workflow. Some provide ‘value adds’ like off-the-shelf data sets, advisory, and algorithms to help others just provide the people capacity.

Customers needing to get data annotated can also do it themselves within their company or crowd-source themselves. There are a variety of Crowdsourcing options available. Customers going down this path just need to manage the process themselves.

Given the amount of processing the AI Builders have to do, they have a need to make this faster and more efficient (let’s call it Annotation AI). They’re constantly looking to apply the AI they’ve built or build new AI to help with annotation. You can, for example, use a large language model to quite accurately classify documents now. Previously, this needed a person. Similarly, image recognition advances mean AI can annotate images to help train another AI without needing a human.

Appen, and data annotation providers, face pressure from multiple directions.

The general Crowdsourcing companies are powerful machines when it comes to winning new customers and growing revenue, particularly in the broad market Appen now finds itself in.

Appen’s original customers, the AI Builders, are heavily incentivised to automate this away (speed to market and cost to a lesser extent) and are continually improving their ability to do so.

But they also have the tailwind of the broad AI Adopter market segment in which all businesses are looking to increase their AI projects.

Go-to-market: Sales Teams and Account Management

Appen uses a sales-led approach to winning business from new customers and account management to expand their existing relationships.

Appen has sales representatives in each of the regions they want to win business, including Australia, the United States, China, Japan and Korea.

They don’t use a self-service sign-up. You have to request a call and quote from a salesperson.

The go-to-market will likely go through a shift as well. The type of account management team you need to manage an $82 million relationship with Google is different to the type of salesperson you need to win $120,000 projects from enterprises.

To get a feel for their go-to-market motion, I applied for a demo with a legitimate use case and haven’t received any contact. In contrast, for another analysis I did, I received a phone call within an hour after submitting a request for a demo form. For a company desperate to grow revenue, it was a little surprising not to hear back quickly.

There is little information about Appen’s go-to-market in publicly published investor information, so I’ve had to infer what is happening from their website, reports, and other sources.

Finances

Appen was a profitable growth machine as recently as 2021. Yet, as the AI Builders have decreased their workloads, Appen’s financial results have turned into a serious problem. As revenues fell, Appen didn’t adjust its expense base, posting a $34m operating loss in 2022.

The Gross Margin held, though. Crowd costs adjusted down with the decrease in revenue. This is promising because it gives a 39-40% gross margin to work with that can scale relatively well with revenue up or down. This margin shows the business has (or can have) underlying resilience.

So what needs to happen with expenses? How can we get profitability and growth happening again?

Splitting the business

Splitting the business might work as a solution going forward. Let’s split the two tracks: the declining business of servicing the AI Builders, and a business for servicing AI Adopters that has signs of market growth.

AI Builders

This business is about servicing the AI Builders, which is primarily about account management and, it seems, some improvements around efficiency.

From the disclosure on the Google contract, we can also see that Google’s contract had only a 26% gross margin. So we can infer that contracts with Meta and any other large remaining AI Builders probably have a lower margin as well.

If we assume that Google, Meta, and Amazon made up 80% of revenue prior to Google ending the contract, then Appen’s AI Builders Business would have $218m in 2023 and something like $191m in 2024.

The probability of further revenue or margin decline in this segment is likely, such as losing another big account or being squeezed on cost respectively. So, the stance here would need to be one of cash flow and profitability through the lowest possible expense base to continue to service the revenue (i.e. no new major product development and no ‘new account’ teams - just focus on what’s in front of you).

AI Adopters

The AI Adopters business is made up of hundreds of customers doing, it seems, smaller projects at higher margins. This business is adding new accounts.

The expense base here likely has a slightly different stance of a mixture of profitability and investment in growth. That investment in growth could be marketing and sales. Given recent performance, this can’t be an overinvestment, though, until the business unit proves itself.

Runway

At the ~$30m loss rate of 2022, Appen’s recent capital raise gives it 12 months of losses of a similar magnitude. Appen says it has cut costs substantially but was still incurring losses as of the last update and may still need to adjust further based on the loss of Google.

Runway is a real concern.