28 ASX Tech Darlings and Their Moats Against AI

Only 3 Moats Helped

Twenty-four ASX tech companies entered February 2026 with what would normally be considered strong strategic positions. The threat of AI meant they were sold off anyway.

On the surface, this looked like an indiscriminate sell-off. But, if you zoom in on this list of well-known, big market-cap companies then the market was a little more selective than it first appeared.

Some moats weren’t punished as hard as others.

This article, the sixth in a series on AI and ASX tech, takes a closer look at the SaaSpocalypse sell-off of the ASX’s largest tech companies to see which moats held up best.

The Cohort: Sold Off ASX Darlings

An earlier article in this series scored 201 ASX-listed tech companies on eight dimensions of defensibility against AI: data, workflow, regulatory, distribution, ecosystem, network, physical and scale. The framework comes from venture capitalist Gokul Rajaram and is what this series refers to as the 8 AI Moats. Each dimension was rated 0 to 3. A score of 2 or higher means the company has a meaningful moat on that dimension.

The 24 companies in focus here fit two criteria. First, they scored 2 or higher on four or more of the eight moat dimensions, putting them among the most defensible technology businesses on the ASX. Second, they were still sold off through the SaaSpocalypse, meaning their three-month share price was down through February 2026.

They span a wide swathe of the sector including B2B SaaS, online marketplaces, data centre operators, IoT and hardware businesses, HealthTech, fintech, proptech, payments, IT distribution, InsurTech, AdTech and consumer apps. The total market cap of the cohort is roughly $71bn, more than double the combined value of the other ASX tech companies we looked at.

The names in the cohort you’d recognise include WiseTech (WTC), Xero (XRO), Pro Medicus (PME), CAR Group (CAR), Computershare (CPU), NEXTDC (NXT), SEEK (SEK), HUB24 (HUB), PEXA (PXA), Life360 (360), Zip (ZIP) and SiteMinder (SDR).

These are not businesses that have significant problems with financial fundamentals. They are the companies a durability-focused investor would expect to be insulated from a sentiment-driven repricing of technology.

Which moats helped defend against the sell-off?

The earlier article’s approach to scoring moats worked for smaller companies but ended up being a misleading way to analyse the Sold-Off Darlings Cohort. Most of these companies score highly on several moats at once because they’ve been able to accumulate moats as they have grown.

This analysis reduces each company to one or two core moats that genuinely describe it. For every company in the cohort we re-scored them by just their primary and secondary moats.

For example, NEXTDC has its physical data centres, PEXA has its government-mandated (regulatory-like) moat, Pro Medicus has its FDA-cleared medical imaging stack. Xero is fundamentally workflow software with an ecosystem on top, not the other way around.

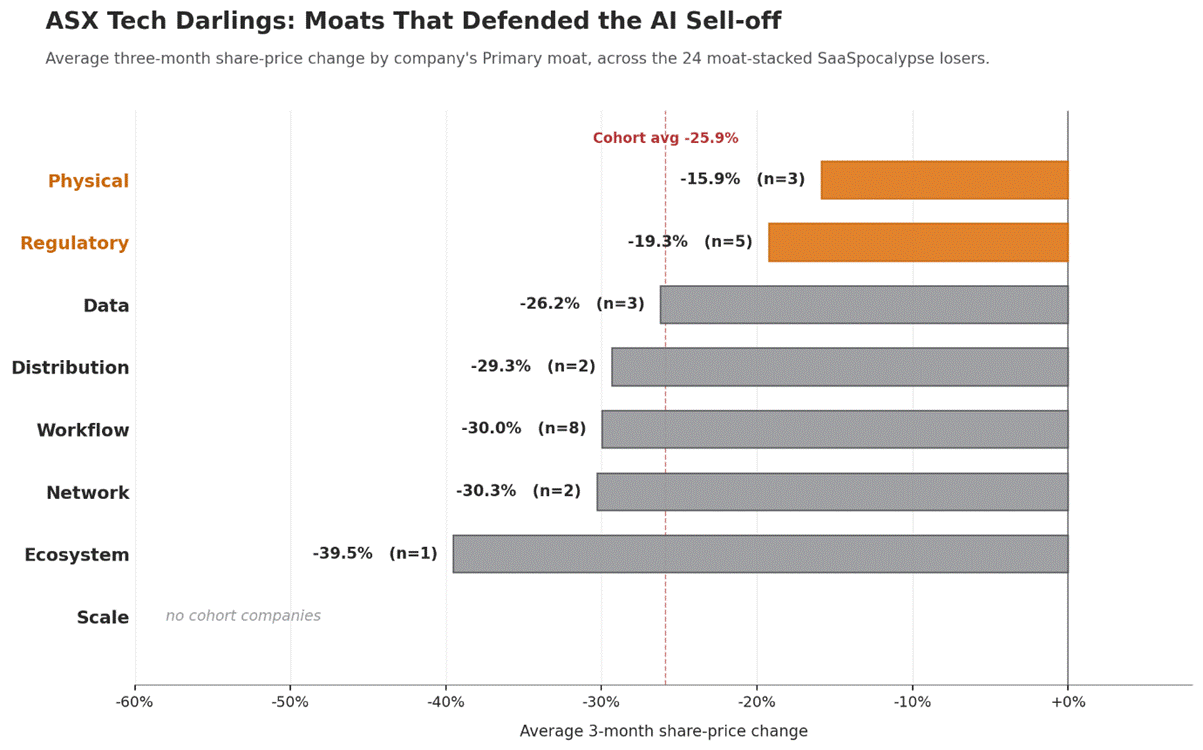

The chart below shows, for each Primary moat, the average three-month share-price change of the cohort companies that carry it.

Figure 1. Average three-month share-price change by Primary moat across the 24 moat-stacked SaaSpocalypse losers.

The insights we can take from this are:

Physical and Regulatory primary moats outperformed the cohort average. The three Physical-primary companies averaged a three-month change of -15.9% and regulatory -19.3%, which is well under the ~-25% average of the overall cohort.

Workflow companies took the bulk of the hit. Workflow is the largest subgroup in the cohort with 8 companies, and they sat below the cohort average at -30.0%. These stereotypical SaaS companies were hit hard. This finding didn’t show up in the initial analysis of moats (because companies of this size have built so many moats) but matches up with what we saw in the small caps.

Other moats did not help. Taken together, the other moats (Data, Distribution, Network, Ecosystem) did not help.

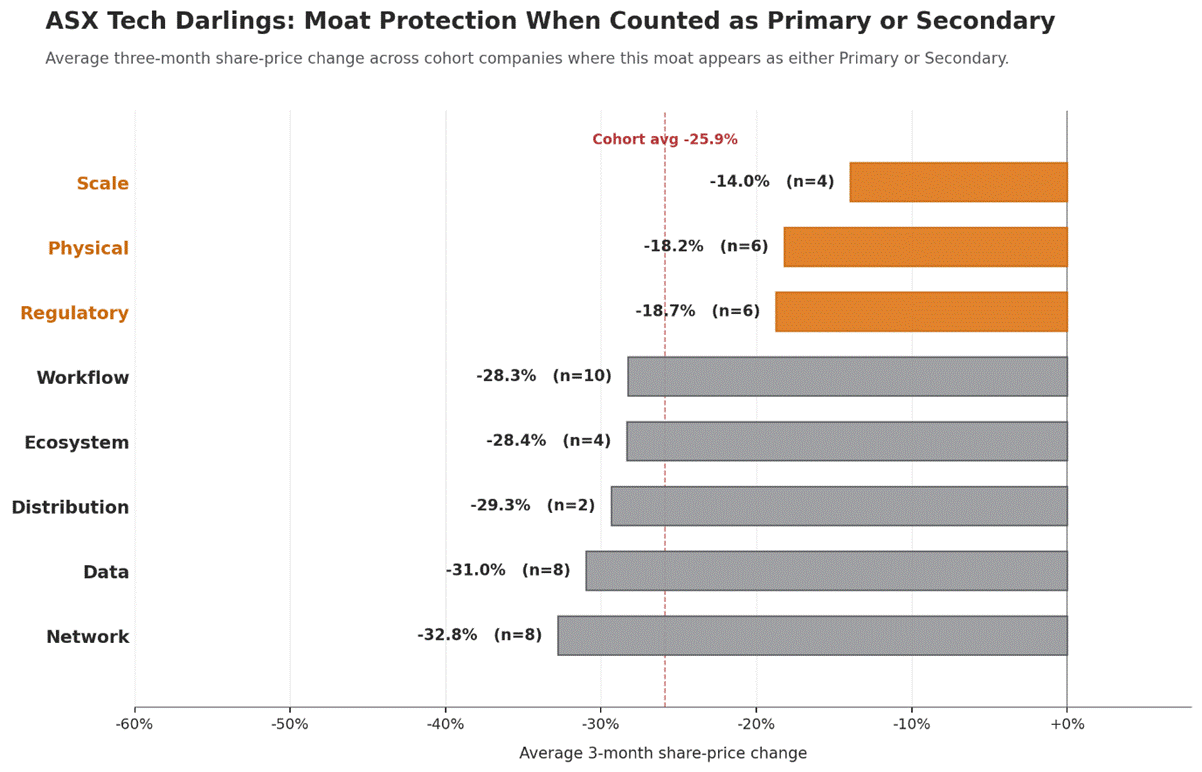

The Primary-or-Secondary view tightens the insights. Physical and Regulatory become even clearer as moats the market favoured. Every other moat, except Scale, was de-rated in SaaSpocalypse (rightly or wrongly). Scale emerged, sensibly, as a strong moat.

How we score the companies

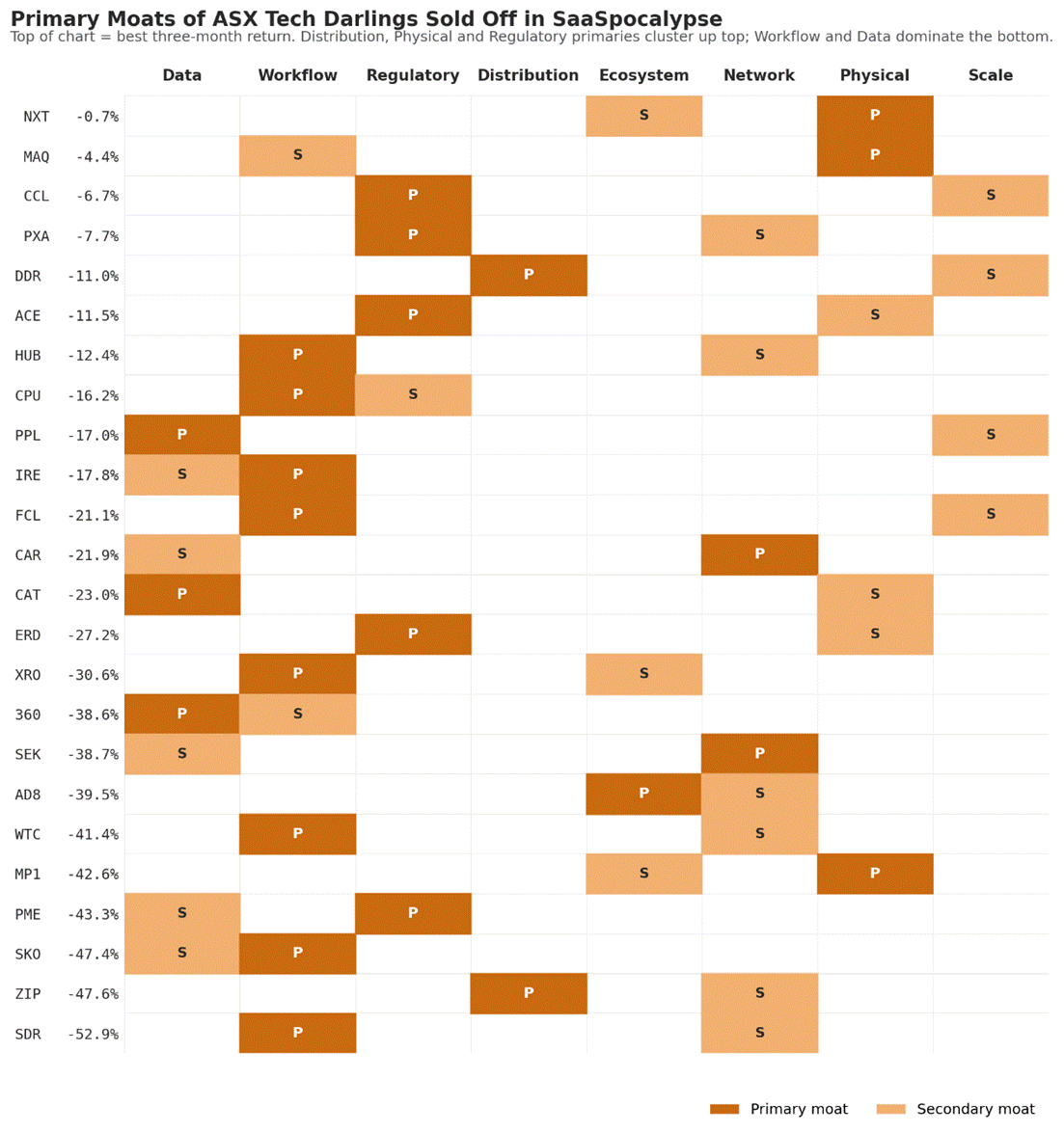

The chart below shows how these ASX tech companies were scored:

Figure 2. Primary (dark) and Secondary (light) moats for each cohort company, sorted top-to-bottom by 3-month return.

The Physical, Regulatory and Scale columns sit mostly at the top of the chart.

Why this might be happening

A reasonable interpretation is that the market is now pricing each moat by how much of its defensibility AI can erode. Here is what the market is probably thinking:

Physical moats describe things AI can’t replicate without help. A data centre is still concrete, fibre, power and a lease. A regulated payments rail still needs cables and rails. AI can make these businesses better, but it can’t bypass them. The market is treating physical moats as the moats AI can’t get to.

Hard-mandate regulatory moats describe legal exclusion that AI doesn’t unwind. PEXA’s monopoly on e-conveyancing does not become less of a monopoly because a foundation model can generate property law text. Cuscal’s settlement rails are not displaced by a more capable agent.

Software-style moats (Workflow, Data, maybe Ecosystem) describe exactly the surfaces AI is best at substituting for. Workflow can be much more easily rebuilt, replaced or superseded by AI. Data used to be, only two years ago, hard to get but now many data sets might be readily replicated or accessed by AI. A software ecosystem used to be a moat against competitors building functionality, now it is not obviously a moat against AI agents that can themselves act as a generic integration layer or produce integrations at close to zero cost.

Whether the market is right to mark these moats down is a separate question. But the direction of the move has a somewhat reasonable basis.

Key Insights

Two takeaways fall out of this:

Workflow, ecosystem or data, that narrative may have stopped working for investors: Continuing to lead with it through 2026 is unlikely to land with investors, however accurate it may be. The harder question is whether your business has or can build the moats the market is still rewarding — physical infrastructure, hard-mandate regulation — and whether those parts of your business are being shown clearly enough to investors. If they don’t exist, the right move is probably honest reframing rather than insisting on a durability claim the market has stopped paying for.

The core moats matter most: The 8 AI Moats framework doesn’t weight each moat equally and the market doesn’t either. Stacking multiple moats doesn’t appear to help in the eyes of the financial markets. The core moats matter more, and the nature of that core moat counts.

It’s worth holding these views lightly as the market might still be wrong. Some moats were punished that seem difficult for AI to replicate (e.g. distribution, network effects). Time will tell what the real answer is.

Next in the series

The next article will be the last in the series. The goal will be to bring together the analysis across each article to hopefully draw some insights we can use as technology investors and executives.